Introduction

Construction bookkeeping isn't just accounting with a hard hat on. Every dollar spent on a job site must be traced to a specific project, crew, phase, and timeline — a level of granularity that standard accounting software and general bookkeeping practices weren't built to handle.

The consequences of getting it wrong are concrete: cash flow shortfalls between project milestones, inaccurate bids that erode margins, IRS compliance failures, and profits that disappear on paper-profitable jobs. According to AICPA data, only 35.9% of construction firms founded in 2011 were still operating by 2022 — a survival rate that reflects, in part, how unforgiving poor financial management can be in this industry.

This guide covers what contractors at every level need to manage their books with confidence:

- What makes construction bookkeeping fundamentally different from standard accounting

- The four core concepts every contractor must understand

- Warning signs that your books need immediate attention

- Practical routines that keep projects financially controlled through closeout

Key Takeaways

- Every cost and revenue line must be tracked at the job level — not just across the company as a whole

- Job costing, revenue recognition, contract retainage, and payroll compliance are the four pillars that separate construction accounting from standard bookkeeping

- Poor bookkeeping creates cash flow gaps, overbilling disputes, and tax exposure that compound quickly

- Structured daily, monthly, and quarterly routines prevent surprises and keep projects audit-ready

- Construction accounting requires industry-specific professionals — general bookkeepers routinely miss the details that matter

Why Construction Bookkeeping Is Different from Standard Accounting

A retail business closes a transaction the same day it opens one. Construction financing doesn't work that way.

A general contractor might be running five projects simultaneously — each with its own budget, subcontractors, timeline, and payment schedule. Revenue comes in through progress billings over months. Costs accumulate unevenly. A single change order can rewrite a project's financial picture overnight.

Three Structural Differences That Matter

| Factor | Standard Business | Construction |

|---|---|---|

| Revenue timing | Point-of-sale | Milestone billings over months/years |

| Cost tracking | Company-wide | Per-project, per-phase, per-crew |

| Financial reports | General P&L | WIP schedules + job cost reports |

Beyond structure, external volatility adds pressure that standard accounting isn't designed to absorb:

- Labor shortages: The 2025 AGC Workforce Survey (n=1,342 firms) found 88% of firms had open craft positions and 41% raised bid prices due to tariffs

- Change orders: AIA research across 11 million contracts found average cost growth from change orders runs approximately 4% of contract value — and that's not an exception, it's the norm

- Multi-state complexity: Crews crossing state lines create separate tax withholding, registration, and compliance obligations that a single-state general ledger won't capture

Standard accounting software is built around the general ledger. Construction bookkeeping is built around the job — and every practice in this guide flows from that difference.

Core Concepts in Construction Bookkeeping

Construction bookkeeping runs on a distinct set of principles tied to the project lifecycle. Understanding these four concepts is the foundation of financial control.

Job Costing

Job costing tracks every dollar spent — labor, materials, equipment, subcontractors, and allocated overhead — to a specific project. The goal: know whether each job made money, and why.

In practice, job costing uses cost codes to tag each transaction to a project and activity type. A concrete pour on Project A gets a different code than electrical rough-in on Project B. When those codes roll up correctly, you get a real-time view of where each project stands against its original estimate.

The stakes are real. A project budgeted at a 12% margin can quietly slide to 7% through poor cost tracking — a $250,000 loss on a $5M contract, per Pronovos analysis of profit fade. That erosion rarely happens all at once. It accumulates through unrecorded expenses, misallocated labor, and change orders that never made it into the books.

WIP (Work-in-Progress) reports are the key output of job costing. They compare estimated vs. actual costs and billings across all active projects, making overbilling and underbilling visible before they become cash flow crises.

Revenue Recognition Methods

Three primary methods apply in construction:

- Cash basis: Record income when payment is received. Simple, but creates distorted pictures on long-running jobs

- Completed contract: Recognize all profit when the project is fully done. Common for short-term jobs; defers tax liability but can mask financial problems mid-project

- Percentage of completion: Recognize revenue proportionally as work progresses. Standard for long-term contracts and required for most GAAP-reporting companies

Under ASC 606, GAAP-compliant companies must evaluate whether revenue is recognized at a point in time or over time based on transfer of control. Most construction contracts qualify for over-time recognition when work is performed on a customer's property or when a specialized asset is being built.

The right method depends on the business's contract mix and tax strategy — a decision best made with a construction-focused CPA.

Contract Retainage

Retainage is the portion of each progress payment — typically 5–10% of contract value — that the project owner withholds until satisfactory completion. It's a contingent asset — not income, not a normal receivable — that can only be collected once specific conditions are met.

Per CFMA-cited data, 10% retainage can exceed the typical 5–6% net profit margin for subcontractors — meaning a subcontractor can finish a job "profitably" and still have negative cash in hand until retainage releases.

Retainage must be tracked separately from regular accounts receivable and recorded as a contract asset on the balance sheet.

State laws vary: California caps public project retainage at 5%, Texas caps at 10%, and most states specify release timelines of 30–60 days after substantial completion.

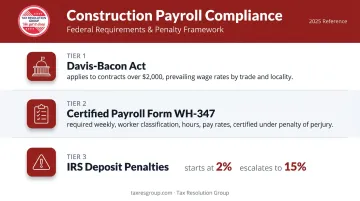

Construction Payroll Complexity

Construction payroll goes well beyond calculating hours and cutting checks. Key compliance layers include:

- Davis-Bacon Act: Applies to all federal or federally-assisted contracts over $2,000; contractors must pay DOL-determined prevailing wage rates by trade and locality

- Certified payroll (Form WH-347): Required weekly on covered projects; must include worker classification, hours, pay rates, and deductions — certified under penalty of perjury

- IRS deposit penalties: Failure to deposit payroll taxes on time carries penalties starting at 2% and escalating to 15% for amounts unpaid after IRS notices

Workers crossing state lines add multi-state withholding and registration requirements. Misclassifying employees as independent contractors — a common shortcut — creates substantial back-tax and penalty exposure. Specialized payroll systems or professional payroll services are the practical solution for contractors with complex crews.

Warning Signs Your Construction Bookkeeping Needs Attention

Inaccurate or Inconsistent Job Costs

If estimated vs. actual reports show large, recurring variances with no clear explanation — or if expenses are being recorded at the company level rather than the job level — job costing has broken down. At that point, project profitability is unknown. Bidding future jobs becomes guesswork.

Cash Flow Surprises and Overbilling Issues

Recurring shortfalls between milestones, difficulty making payroll on time, or clients disputing invoice amounts all point to the same root cause: billing and retainage aren't being tracked against actual progress.

A current WIP report should always show how much has been earned vs. billed across every active project. If that report doesn't exist or is months old, overbilling disputes and cash flow crises are only a matter of time.

Tax and Compliance Errors

Common red flags include:

- Missed payroll tax deadlines

- Incorrect or missing 1099-NEC filings for subcontractors

- Year-end tax surprises from data captured too late or in the wrong format

These errors don't stay small. IRS penalties compound, and state agencies act quickly on late filings.

Best Practices and Tips for Construction Bookkeeping

Separate Finances and Use Multiple Bank Accounts

Keep business and personal finances completely separate. Beyond that basic discipline, consider dedicated accounts for:

- Operating expenses

- Payroll funding

- Tax reserves

This prevents commingling, simplifies reconciliation, and makes it far easier to see where cash actually stands at any point in a project cycle.

Implement Job Costing from Day One

Set up your chart of accounts and assign cost codes before a project begins — not after expenses start accumulating. Once transactions are miscoded or posted at the company level, correcting them retroactively is time-consuming and error-prone. Getting the structure right at project setup is the single highest-leverage bookkeeping decision a contractor can make.

Establish a Consistent Invoicing and Retainage Process

- Send invoices on a fixed schedule tied to project milestones

- Clearly separate retainage from billable amounts on every invoice

- Track receivables aging weekly and follow up before payments become 60+ days overdue

Slow-paying clients are a cash flow problem in waiting. A retainage schedule that isn't tracked proactively can leave significant money uncollected months after project closeout.

Reconcile Accounts and Back Up Records Regularly

Bank reconciliation should happen monthly at minimum — comparing internal records against actual bank statements to catch errors, duplicate entries, or unauthorized transactions. For data protection, follow the NIST/NCCOE 3-2-1 backup rule: 3 copies of financial records, on 2 different storage types, with 1 stored offsite.

Work with Accounting Professionals Who Understand Construction

Once you're managing job costing, retainage, certified payroll, and multi-state tax obligations simultaneously, the bookkeeping complexity outpaces what general accounting support can handle. Revenue recognition rules and compliance requirements specific to construction require expertise that goes well beyond standard bookkeeping.

Firms like Tax Resolution Group, with deep QuickBooks expertise and experience serving contractors across California and beyond, can provide setup, payroll support, and tax planning tailored to construction-specific needs. For smaller and mid-sized contractors who don't need full-time in-house accounting staff, professional support at a flexible engagement level is often more cost-effective than hiring dedicated staff.

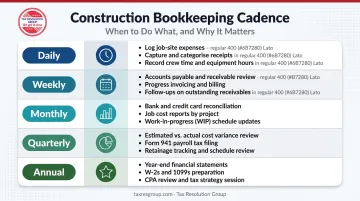

Creating a Consistent Construction Bookkeeping Routine

Bookkeeping is not a once-a-year task. A structured cadence ensures nothing slips across active projects. Use this framework as a recurring reference — each frequency tier targets the tasks most likely to cause problems if delayed.

| Frequency | Key Tasks |

|---|---|

| Daily | Log expenses with correct cost codes, capture receipts, record time by job site |

| Weekly | Review accounts payable and receivable, send invoices for completed milestones, follow up on overdue payments |

| Monthly | Reconcile all bank and credit card accounts, run job cost reports and WIP summaries, review payroll compliance |

| Quarterly | Compare estimated vs. actual performance across all projects, file Form 941 (payroll tax deposits due April 30, July 31, October 31, January 31), assess retainage balances due |

| Annual | Prepare year-end financial statements, issue W-2s and 1099-NECs by January 31, review revenue recognition method with a CPA, plan for upcoming project bids |

Consistency matters more than getting every entry perfect on the first try. Contractors who follow this cadence avoid cash flow surprises, catch retainage gaps before they become disputes, and show up to audits with records already in order.

Frequently Asked Questions

What is the best accounting method for construction companies?

Most construction companies use the percentage of completion method for long-term contracts, since it matches revenue to work actually performed over time. The completed contract method fits shorter jobs with clear endpoints. A construction CPA should help match the method to your contract types, business size, and tax strategy.

What does a construction bookkeeper do?

A construction bookkeeper tracks job costs, manages accounts payable and receivable, processes payroll (including certified payroll when required), and reconciles bank accounts. They also produce job cost analyses and WIP reports to keep each project financially on track.

What is the best accounting program for construction?

Popular options include QuickBooks Online for smaller contractors, Foundation Software for built-in certified payroll and WIP reporting, and Sage 300 CRE for larger commercial firms. The right choice depends on company size, payroll complexity, and reporting needs — proper setup matters as much as the software itself.

What is contract retainage in construction?

Retainage is the percentage of payment — typically 5–10% — withheld by the project owner until work is completed to their satisfaction. It must be recorded as a contract asset on the balance sheet, not as income, until the contractor has an unconditional right to collect it.

How does job costing work in construction bookkeeping?

Job costing assigns every expense, labor, materials, subcontractor payments, and overhead, to a specific project using cost codes. This lets contractors compare actual spending against estimates in real time and measure the true profitability of each job.

Should I hire a bookkeeper or outsource construction bookkeeping?

In-house bookkeepers integrate closely with daily operations but carry salary and training costs year-round. Outsourcing to a specialized firm gives access to construction accounting expertise at a more flexible cost, making it a practical fit for small to mid-sized contractors who don't need full-time support.