Bookkeeping gets recommended constantly, but the practical case for it rarely gets made clearly. "Keep good records" is advice without teeth. What actually matters is understanding how consistent bookkeeping changes tax outcomes — filing speed, deduction capture, audit exposure — and what it costs when it doesn't happen.

This guide makes that case directly.

Key Takeaways

- Organized bookkeeping turns tax season into an execution task rather than a reconstruction project

- Year-round expense tracking is the primary mechanism for capturing every eligible deduction

- Clean financial records reduce audit risk and shorten resolution timelines if scrutiny does arrive

- Neglected bookkeeping doesn't just create stress — it creates penalties, missed credits, and financing complications

- Integrating bookkeeping with tax preparation cuts the reclassification work that drives up filing costs

What Is Bookkeeping and Why It Matters for Taxes

Bookkeeping is the ongoing process of recording, categorizing, and reconciling every financial transaction a business makes — sales, expenses, payroll, asset purchases, contractor payments, and more. Done consistently, it produces the financial records that everything else depends on.

Tax preparation sits downstream of bookkeeping. A tax preparer uses income statements, balance sheets, and categorized expense records to complete a return accurately. Without reliable records, even the most experienced tax professional is working with incomplete information — and incomplete information produces incomplete returns.

Bookkeeping is also a control mechanism — one that gives business owners a real-time view of their financial position throughout the year, not just in the weeks before a deadline. That ongoing visibility makes three things possible that reactive recordkeeping simply cannot:

- Proactive tax planning before year-end deadlines

- Accurate estimated quarterly payments that avoid underpayment penalties

- Confident financial decisions backed by current, reliable data

Key Advantages of Bookkeeping for Tax Preparation

The advantages below focus on concrete, operational outcomes — the kind that affect filing timelines, tax liability, error rates, and audit exposure.

Advantage 1: Organized Records Eliminate Last-Minute Filing Chaos

When transactions are recorded and categorized consistently throughout the year, tax season becomes an execution task. The financial statements a tax preparer needs — income statements, balance sheets, payroll records — are already structured and accessible. Nothing needs to be reconstructed.

In practice, this means monthly reconciliation, categorized expense accounts, and up-to-date ledgers. When a tax preparer sits down with those records, the data is ready. When they don't exist, the preparer bills for cleanup first.

That cost is real. According to the NSA Income and Fees Survey, 75.1% of tax preparers charge more for disorganized or incomplete paperwork, with an average added fee of $145.14 just to complete a sole proprietor return. That's before counting the time the business owner spends locating documents.

The time burden extends beyond filing season. NSBA's 2024 survey found that the majority of small business owners spend more than 20 hours per year dealing with federal taxes — and 90% said federal taxes directly impact day-to-day operations.

This advantage matters most for:

- Businesses with 50+ monthly transactions

- Companies with multiple revenue streams

- Owners transitioning business structures (LLC to S Corp, for example)

- Anyone who has filed an extension in the past due to missing records

Advantage 2: Year-Round Expense Tracking Maximizes Deductions

Deductible expenses don't wait for tax season — they happen every day. A meal with a client, a software subscription, a vehicle mile driven for business, a home office used exclusively for work. Without a system that captures and categorizes these expenses as they occur, they disappear.

Bookkeeping that records expenses in real time translates directly into deduction capture. When expenses are logged under the correct accounts throughout the year, a tax preparer can cross-reference those categories against IRS-eligible deductions without digging through raw bank statements.

The IRS requires that expense records identify the payee, amount paid, proof of payment, date incurred, and a description confirming it was a business expense — bookkeeping creates that documentation automatically.

Common deduction categories that require consistent tracking include:

- Home office and rent expenses

- Vehicle and travel costs

- Equipment purchases and depreciation (including Section 179 elections)

- Contractor payments (which also trigger 1099 requirements)

- Employee salaries, benefits, and payroll taxes

- Business insurance, legal, and professional service fees

- Advertising, marketing, and software subscriptions

Without categorized records, many of these deductions get missed — not because the expenses weren't legitimate, but because they can't be substantiated. The IRS standard is clear: expenses must be "ordinary and necessary" and properly documented to be deductible.

Industries with varied expense types — construction, media and entertainment, contracting, and retail — see the highest impact here, where deductible expenses span multiple categories and are easy to misclassify without a structured system.

Advantage 3: Built-In Audit Readiness Reduces IRS Risk

An IRS audit doesn't announce itself in advance. Businesses with accurate, documented bookkeeping records are in a defensible position from day one. Those without organized books face a reactive scramble to reconstruct documentation under pressure — often for transactions that happened years ago.

The IRS selects returns for audit through random screening and computer comparison against statistical norms, as well as through related examinations involving business partners or investors.

Inconsistencies between reported income, claimed deductions, and filed financial statements are common audit triggers — all of which trace back to poor bookkeeping.

Audit-ready bookkeeping includes:

- Bank statements reconciled monthly against the general ledger

- Receipts matched to every expense entry

- Properly classified transactions with supporting documentation

- 1099 forms filed for all qualifying contractor payments

- Financial statements that are consistent across all reporting periods

The IRS requires businesses to retain records for at least 3 years from the filing date — and up to 6 years if income was underreported by more than 25%. That retention window is a legal requirement, not a guideline.

Tax Resolution Group provides IRS audit representation for clients who need it. In those situations, having clean bookkeeping records already in place — rather than reconstructing them under deadline — significantly narrows the scope of what an auditor can question.

This matters most for businesses that:

- Claim significant deductions relative to revenue

- Work with multiple independent contractors

- Have experienced rapid revenue growth

- Have previously filed amended returns

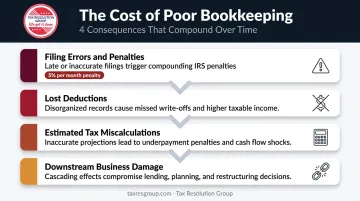

What Happens When Bookkeeping Is Ignored

Neglected bookkeeping sets off a chain of financial problems that compounds well before tax season arrives.

Filing errors and penalties. Missing transactions, misclassified expenses, and unreconciled accounts increase the likelihood of errors on filed returns. The IRS failure-to-file penalty is 5% of taxes owed per month, up to 25% — and inaccurate records are a direct pathway to underpayment, interest charges, and notices.

Lost deductions. When expenses aren't tracked in real time, business owners face a binary problem: they either miss claiming legitimate deductions (because they can't substantiate them) or incorrectly claim expenses they can't prove. Both outcomes cost money.

Estimated tax miscalculations. Quarterly estimated payments depend on knowing current-year income. Without up-to-date books, those calculations are guesswork — and underpayment triggers its own penalty structure from the IRS.

Downstream business damage. Poor financial records create problems beyond tax filing:

- Lenders require reliable financial statements for loan approval — disorganized books can disqualify a business from financing it would otherwise qualify for

- Growth decisions become guesswork without accurate P&L and cash flow data

- Entity structure changes (like converting to an S Corp) require clean historical records to execute properly

A larger tax bill is only the most visible consequence. Disorganized books affect lending eligibility, strategic planning, and the ability to restructure — costs that accumulate long after the return is filed.

How to Get the Most Value from Your Bookkeeping

Bookkeeping delivers its full value when practiced consistently — monthly at minimum — reviewed against actual bank statements, and aligned with the chart of accounts a tax preparer uses. Records that are already structured the way a tax return requires don't need manual reclassification at filing time. That alignment alone reduces both the time and cost of tax preparation.

Software like QuickBooks can automate transaction categorization, flag discrepancies, and generate the financial reports — P&L, balance sheet, cash flow statement — that tax preparers rely on. Tax Resolution Group's QuickBooks expertise means clients get setup, training, and ongoing support connected directly to tax outcomes, not just data entry.

That support goes beyond data entry. The firm's approach treats bookkeeping as the foundation for corporate strategy — prioritizing long-term planning over routine recordkeeping.

When transaction volume grows or income streams multiply, that strategic foundation becomes critical. Businesses with complex expense structures benefit most from a firm that handles both bookkeeping and tax preparation under one roof:

- The same team that categorizes transactions also files the return

- Reclassification errors at year-end are eliminated before they happen

- Tax strategy adjustments can be made in real time, not retroactively

Tax Resolution Group offers both services as part of a unified engagement — which means the information gaps that inflate costs and introduce errors don't get the chance to develop.

Conclusion

Bookkeeping's value in tax preparation shows up in concrete outcomes: faster filing, lower tax liability, stronger audit protection, and less financial stress across the business. Each of these results traces directly back to having organized, accurate records when tax obligations come due.

The advantages compound over time. Each year of consistent bookkeeping makes the next tax season more manageable and the financial picture clearer for planning and growth decisions.

Bookkeeping is an ongoing financial practice, not a seasonal task or a one-time cleanup. Businesses that maintain it year-round file faster, face fewer surprises, and carry more confidence into every financial decision they make.

Frequently Asked Questions

Are bookkeeping services a tax write-off?

Yes. IRS Publication 334 confirms that fees paid to accountants and bookkeepers are deductible as ordinary and necessary business expenses when directly related to operating the business. Confirm the specifics of your situation with a qualified tax professional.

Do tax preparers do bookkeeping?

Some do. Working with a firm that handles both functions under one engagement reduces errors and eliminates the reclassification work that happens when separate providers use different account structures. Tax Resolution Group, for example, provides both services together — which means your books and your return are built on the same account structure from the start.

What are the benefits of bookkeeping?

Accurate financial records, maximum deduction capture, audit-ready documentation, and better cash flow visibility — all of which lead to a faster and more accurate tax filing process. Consistent bookkeeping also gives you reliable numbers to act on when evaluating pricing, hiring, or growth decisions throughout the year.

How often should I update my bookkeeping records for tax purposes?

Monthly is the standard for most small businesses. Monthly reconciliation prevents errors from accumulating, keeps records accurate for quarterly estimated payments, and ensures books are tax-ready at year-end without a major cleanup effort.

What documents do I need for bookkeeping and tax preparation?

Core documents include:

- Bank and credit card statements

- Receipts for business expenses

- Invoices issued and received

- Payroll records

- 1099 forms for contractors

- P&L statement and balance sheet

- Asset purchase records for depreciation purposes

Can poor bookkeeping lead to an IRS audit?

Yes. Inconsistent income reporting, unsupported large deductions, and financials that don't reconcile with your filed return are red flags in the IRS's automated screening process — all common outcomes of poor bookkeeping. Organized records won't prevent scrutiny, but they put you in a defensible position if it comes.