This guide walks through the four main IRS tax resolution options — installment agreements, offers in compromise, currently not collectible status, and penalty abatement — so you can understand which path might fit your circumstances and what to expect from each one.

Key Takeaways

- Ignoring an IRS balance triggers escalating penalties, interest, liens, and levies; acting early preserves more resolution options

- Four main programs exist: installment agreements, OIC, CNC status, and penalty abatement

- The Offer in Compromise has strict qualification criteria — the IRS accepted only 5,464 of 38,797 proposals in FY 2025

- Filing all unfiled returns is a prerequisite for most resolution programs

- California taxpayers may also owe the Franchise Tax Board separately — both tracks need attention

What Happens If You Don't Pay the IRS

Ignoring a tax bill doesn't make it go away. The IRS follows a structured collection process that escalates in predictable stages, and the longer you wait, the more expensive the problem becomes.

Penalties and Interest Add Up Fast

Two separate penalties begin immediately:

- Failure-to-file penalty: 5% of unpaid tax per month, capped at 25%. For returns filed more than 60 days late after December 31, 2025, the minimum penalty is $525 or 100% of the unpaid tax, whichever is less.

- Failure-to-pay penalty: 0.5% of unpaid tax per month, also capped at 25%

On top of penalties, interest compounds daily at the federal short-term rate plus 3%, and it adjusts quarterly. A $10,000 balance can reach $13,000 or more within a year from penalties and interest alone.

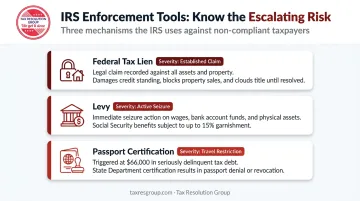

Liens, Levies, and Passport Consequences

The IRS has two primary enforcement tools, and they work very differently:

| Tool | What It Does |

|---|---|

| Federal Tax Lien | A legal claim against your property (home, car, financial accounts). The IRS files a public Notice of Federal Tax Lien, damaging your credit and blocking property sales or new loans. Nothing is seized — but the lien follows you. |

| Levy | The actual seizure. The IRS can garnish wages, pull funds from bank accounts, or seize assets without going to court. Up to 15% of Social Security benefits can be levied through the Federal Payment Levy Program. |

| Passport Certification | If your debt exceeds $66,000 (the 2026 "seriously delinquent" threshold, including penalties and interest), the IRS can certify your debt to the State Department, triggering passport denial or revocation. |

IRS Tax Resolution Options When You Can't Pay

The IRS built these programs for taxpayers who genuinely cannot pay their full balance. Which one fits your situation depends on your income, assets, monthly expenses, and how those figures compare against your outstanding debt.

IRS Installment Agreements (Payment Plans)

An installment agreement lets you pay your tax debt over time in monthly installments. Two main structures exist:

- Short-term plan: Pay within 180 days; available when you owe less than $100,000 in combined tax, penalties, and interest

- Long-term plan: Monthly payments for up to 72 months; available when you owe $50,000 or less

For smaller balances, many taxpayers can apply directly through IRS.gov Payment Plans without extensive financial disclosure.

Two things to know before you apply:

- Penalties and interest keep accruing throughout the agreement, so your total paid will exceed your original balance

- The IRS is generally prohibited from levying while an agreement is pending, in effect, or for 30 days after rejection or termination — which halts the most aggressive collection activity

Offer in Compromise (OIC)

An OIC is a formal agreement that lets eligible taxpayers settle their tax debt for less than the full amount owed. The IRS evaluates your "reasonable collection potential" — a calculation based on your income, allowable expenses, and asset equity — to determine what you can realistically pay.

Eligibility prerequisites:

- All required tax returns must be filed

- You must have received a bill for at least one tax debt

- Current estimated tax payments must be up to date

- No open bankruptcy proceeding

The IRS offers a free OIC Pre-Qualifier Tool to help taxpayers assess whether they might qualify before applying.

Here's the honest reality: in FY 2025, the IRS accepted just 5,464 of 38,797 proposed offers. This program has genuinely strict criteria, which is exactly why it's frequently exploited by scam companies making promises they can't keep (more on that below).

Currently Not Collectible (CNC) Status

CNC status is a temporary pause on all IRS collection activity. The IRS grants it when your allowable monthly expenses equal or exceed your income — meaning paying anything toward your tax debt would leave you unable to cover basic living costs.

What CNC is not: debt forgiveness. Interest and penalties keep accruing the entire time. The IRS reviews your finances each year when you file and can reactivate collection if your income improves.

The strategic value is real, though. For taxpayers in genuine short-term hardship, CNC buys time without the threat of levies — and since the IRS has a 10-year collection statute, time itself can work in your favor in some cases.

Penalty Abatement

Penalties can represent a significant portion of what you owe, and the IRS can reduce or remove them under two circumstances:

First-Time Penalty Abatement (FTA) applies if you have a clean three-year compliance history: no prior unreversed penalties on the same return type, all required returns filed, and the tax paid or in a payment arrangement. It covers failure-to-file, failure-to-pay, and failure-to-deposit penalties.

Reasonable Cause Relief applies when circumstances outside your control — serious illness, natural disaster, a death in the immediate family, or inability to obtain records — prevented timely filing or payment. The IRS evaluates each case individually.

One important boundary: interest is only reduced when it's directly tied to a penalty being removed. Penalty abatement doesn't independently eliminate underpayment interest.

Which IRS Resolution Option Is Right for Your Situation?

Here's a practical framework based on your financial circumstances:

| Your Situation | Option to Explore |

|---|---|

| You can afford monthly payments over time | Installment Agreement |

| You genuinely cannot pay the full amount and meet strict financial criteria | Offer in Compromise |

| Paying anything would prevent covering basic living expenses | Currently Not Collectible Status |

| Penalties are driving up your balance significantly | Penalty Abatement Request |

These options aren't mutually exclusive. Penalty abatement, for example, can be combined with an installment agreement — reducing the total balance before setting up the payment plan. Applying for the wrong program, though, can result in rejection and restart active IRS collection.

File all unfiled returns first. Most IRS resolution programs require this, and filing — even when you can't pay — demonstrates good faith and unlocks access to relief options. Continuing to not file makes every path forward harder to pursue.

Once your federal strategy is clear, don't overlook state obligations. California residents: the Franchise Tax Board operates entirely independently from the IRS, with its own collection timelines, resolution programs, and enforcement tools. State and federal balances must be addressed on separate tracks — resolving one doesn't resolve the other.

Warning Signs of Tax Relief Scams

The IRS's 2026 Dirty Dozen list specifically warns about OIC mills — companies that advertise "settle for pennies on the dollar," charge large upfront fees, and submit applications they know will fail. The problem is widespread enough that in June 2026, the FTC and Nevada reached a settlement requiring tax-relief scammers to surrender nearly $10 million in cash and assets.

Clear red flags to watch for:

- Guarantees of a specific settlement outcome before reviewing any financial documents

- High-pressure tactics demanding immediate action or payment

- Full fee payment required before any work begins

- Unwillingness to disclose or verify professional credentials

- Discouraging you from communicating directly with the IRS

Only three types of professionals have unlimited rights to represent taxpayers before the IRS: Enrolled Agents (EAs), Certified Public Accountants (CPAs), and tax attorneys. Before hiring anyone, verify their credentials using the IRS Directory of Federal Tax Return Preparers.

When to Get Professional Help with Tax Resolution

Smaller, straightforward situations — like setting up a basic installment agreement for a manageable balance — can often be handled directly through IRS.gov. But the complexity changes quickly when:

- Your balance is large or spans multiple tax years

- You have unfiled returns

- An active lien or levy is in place

- You're pursuing an Offer in Compromise

- You need audit representation

In these cases, professional representation handles all IRS communications on your behalf. A missed response deadline can restart the clock on penalty accrual, and an improperly documented OIC application is typically returned without processing — forcing you to start over.

That's where having the right team changes the outcome. Tax Resolution Group works with individuals and small businesses in Huntington Beach and across California to evaluate your options, match you to the right IRS program, and manage the negotiation process from start to finish. To discuss your situation with a qualified professional, reach out at (714) 657-3155 or info@taxresgroup.com.

Frequently Asked Questions

What is a tax resolution?

Tax resolution is the process of using official IRS programs: installment agreements, offers in compromise, currently not collectible status, and others — to settle or manage unpaid tax debt. State tax agencies like California's Franchise Tax Board operate similar programs.

How long does a tax resolution take?

Timelines vary significantly by program. Installment agreements for smaller balances can be set up online within days. An Offer in Compromise typically takes six months to over a year for the IRS to review and accept or reject.

Why am I getting calls about a tax resolution?

Unsolicited calls offering tax resolution services are almost always from third-party companies, not the IRS. The IRS communicates primarily by mail. Be cautious of any high-pressure call claiming it can reduce your tax debt immediately.

Can the IRS garnish my wages if I set up a payment plan?

Once an installment agreement is approved and in good standing, the IRS generally suspends wage garnishments and other levies. Missing payments can void the agreement and restart collection activity — and the IRS typically does not offer second chances on lapsed agreements.

What is the difference between a tax lien and a tax levy?

A lien is a legal claim against your property that affects your credit and ability to sell assets or obtain loans. A levy is the actual seizure: garnishing wages, withdrawing from bank accounts, or seizing other property.

Can I negotiate with the IRS directly without a professional?

Taxpayers can contact the IRS directly and apply for installment agreements or other standard programs online. Complex cases — large balances, unfiled returns, or offers in compromise — carry significantly more risk and generally benefit from professional representation.