Introduction

Most business owners spend decades building something valuable — and less than an afternoon thinking about what happens to it when they step away. That gap is costly.

According to a Gallup survey of 1,264 US business owners, 33% have no long-term plan or are unsure about their business's future. Meanwhile, 52.3% of employer businesses are owned by someone age 55 or older — meaning succession isn't a distant concern for most owners. It's a near-term reality.

Business succession planning is the process of identifying, preparing, and legally structuring who will take over a business when an owner retires, becomes incapacitated, or passes away. A solid plan protects business value, minimizes taxes, and prevents family conflict. Without one, everything an owner spent years building can unravel quickly.

That's what this guide addresses. It delivers a complete, step-by-step checklist covering leadership, ownership, legal, financial, and tax components of a succession plan — written for small and mid-sized business owners, family business operators, and entrepreneurs who want to protect what they've built.

Key Takeaways

- Succession planning protects the business from unexpected death, disability, or forced departure — not just retirement

- A complete plan addresses four pillars: leadership transition, ownership transfer, business valuation, and tax and estate planning

- Most plans fail because owners start too late or build the plan without qualified advisors

- Succession and estate planning overlap directly — business assets are often a family's largest source of personal wealth

- Starting early expands your options to reduce tax exposure and transfer business value on your own terms

Why Business Succession Planning Matters

Many business owners treat succession as something to handle eventually. The data says eventually arrives faster than expected.

Deloitte's 2026 survey of 300 family business executives found that 78% expect a CEO transition within 10 years and 42% expect one within three to five years — yet only 23% are actively implementing a succession plan. The gap between expectation and preparation is where businesses get into serious trouble.

The Risks of Going Without a Plan

When an owner exits without a documented plan, the consequences hit fast:

- Heirs or partners may be forced to sell at unfavorable prices when no clear terms exist

- Co-owners and family members dispute authority without a documented agreement to reference

- Key clients and employees leave when leadership uncertainty signals instability

- Unplanned transfers trigger capital gains and estate taxes that structured planning could have reduced

The Estate Tax Reality

When a business is a family's primary asset, heirs may face a substantial estate tax bill with no liquid cash to pay it. The 2026 federal estate tax basic exclusion amount is $15,000,000 per the IRS, with a top marginal rate of 40% on taxable amounts. For business-heavy estates above that threshold, this is not a theoretical risk — it's a liquidity problem.

Addressing this exposure through structured planning — buy-sell agreements, life insurance trusts, or gifting strategies — is exactly what separates a managed transition from a forced one. Beyond the tax math, a documented succession plan signals stability to employees, lenders, customers, and partners. It preserves business value during the transition, not just after it.

The Business Succession Planning Checklist

This checklist is phased and actionable. Not every step applies to every situation, but covering all areas is the baseline for a complete plan.

Step 1: Define Your Succession Goals and Timeline

Start with the fundamental questions:

- Do you want to keep the business in the family, or sell to a partner or outside buyer?

- Are you planning a gradual phase-out or a clean break?

- What's your target timeline — even a tentative one?

A timeline gives every downstream decision a deadline. Without one, succession planning tends to stay perpetually "in progress" while the business and its owner keep aging.

Step 2: Identify and Evaluate Potential Successors

Successors can come from three places: family, existing employees or partners, or the open market. The right choice depends on:

- Whether they can run the business operationally, not just own it on paper

- Whether they actually want the role — reluctant successors create their own problems

- Whether clients, employees, and vendors already respect them

Evaluate more than one candidate when you can. Concentrating all succession hopes on a single person is its own kind of risk.

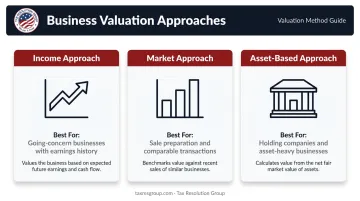

Step 3: Conduct a Professional Business Valuation

An accurate valuation is the foundation of everything else. It determines:

- The price for a buy-sell agreement

- The basis for any gifting strategy

- Estate planning figures for tax purposes

- What's actually driving the business's worth (customer concentration, intellectual property, recurring revenue, key personnel)

The three standard valuation approaches:

| Approach | Best Used For |

|---|---|

| Income | Going-concern businesses with earnings or cash flow history |

| Market | Sale preparation and comparable private-company transactions |

| Asset-based | Holding companies, asset-heavy businesses, or firms with limited earnings history |

IRS Revenue Ruling 59-60 governs closely held business valuation for estate and gift tax purposes — it's not optional guidance; it's the standard the IRS applies. Tax Resolution Group offers business valuation services for owners who need an objective, defensible assessment that holds up for estate planning, buy-sell agreements, and gift strategies.

Step 4: Draft and Fund a Buy-Sell Agreement

A buy-sell agreement is a legally binding contract that defines what happens to an ownership interest when a triggering event occurs — death, disability, retirement, bankruptcy, or departure.

Key decisions within the agreement:

- Mandatory vs. optional — mandatory agreements offer stronger protection for heirs and remaining owners, eliminating room for dispute

- Funding mechanism — life insurance, installment payments, or a sinking fund (a dedicated reserve account); the agreement means nothing if there's no money to execute it

The Supreme Court's ruling in Connelly v. United States held that corporate-owned life insurance proceeds can increase the taxable value of a deceased shareholder's interest. Corporate redemption structures now carry estate tax valuation risk — how the insurance is owned and how the agreement is drafted both require careful attention.

Step 5: Create a Training and Development Plan for the Successor

Naming a successor is just the start. A structured development plan should:

- Identify specific skills gaps

- Assign increasing management responsibility over time

- Set a knowledge-transfer timeline with milestones

- Include introductions to key clients, vendors, and lenders

A visible development plan also gives employees and customers confidence that the transition is deliberate, not a scramble.

Step 6: Address Estate Planning and Ownership Transfer Structures

Ownership transfer must be legally structured. Common vehicles include:

- Family limited partnerships (FLPs) — allow minority interest discounts that reduce the taxable value of gifted interests, though IRS Section 2036 scrutiny requires real governance purpose

- LLCs — flexible and commonly used for transfer planning with similar discount potential

- Irrevocable trusts (IDGTs, GRATs) — allow transfers of future appreciation out of the taxable estate; IDGTs are complete for transfer tax purposes but taxable to the grantor for income tax, which has its own planning implications

- Annual gifting — the 2025 annual gift tax exclusion is $19,000 per donee, a simple and reliable tool when used consistently over time

Coordinate the succession plan with the owner's revocable trust and beneficiary designations. Misalignment between these documents creates exactly the disputes succession planning is meant to prevent.

Step 7: Communicate the Plan to Key Stakeholders

Once the plan is documented, communicate it — selectively and strategically:

- Family members should understand the broad structure, even if not every financial detail

- Key employees need to know a plan exists and who leads the business going forward

- Lenders and major clients benefit from knowing continuity is planned

Disclosure levels will vary by audience. The goal isn't full transparency — it's enough information to prevent uncertainty from becoming a retention or relationship problem.

Step 8: Review and Update the Plan Annually

A succession plan written once and filed away is a liability, not a protection. Trigger a review when:

- Tax law changes (estate tax exemptions, gift limits, entity rules)

- Business value shifts significantly

- A named successor changes their plans

- A major personal or family event occurs

At minimum, schedule a formal annual review with your advisory team.

Key Financial and Tax Considerations

Estate and Gift Tax Planning

The federal estate tax exemption sits at $13.99 million per individual in 2025 — but the TCJA provisions governing that figure are scheduled to sunset after 2025, potentially cutting it roughly in half. Owners with business-heavy estates near or above that threshold should structure transfers well before death, not after.

Effective tools for reducing taxable transfer values:

- Annual gifting programs — $19,000 per donee per year (2025) adds up significantly over a decade

- FLP and LLC minority interest discounts — transferred interests may qualify for lack-of-control and lack-of-marketability discounts, reducing their taxable value

- Installment sales to IDGTs — allow the owner to transfer future business appreciation while receiving a structured payment stream

Retirement Income Planning

For owners whose personal wealth is largely tied up in the business, the succession plan must also address personal financial security. Options include:

- Installment sales — structured payments over time from the buyer (successor)

- Deferred compensation arrangements — pre-planned income the business pays post-exit

- Structured buyouts — designed to fund the owner's retirement without stripping the business of capital the successor needs

Planning for the owner's post-exit income is not secondary to the transfer — it's part of the same decision.

Liquidity Planning

Life insurance is the most common tool for funding a buyout when a triggering event occurs. Without it, the business or surviving owners may face a cash shortfall at the worst possible moment. Liquidity gaps are among the most common causes of succession plan failure. Getting ahead of this requires mapping out both tools and timing.

Common funding mechanisms include:

- Life insurance policies — entity-owned or cross-owned, structured to pay out at a triggering event

- Cross-purchase agreements — co-owners fund each other's buyout through individually held policies

- Entity-redemption plans — the business itself holds policies and redeems the departing owner's interest

Tax Resolution Group helps business owners map out the full tax picture of a succession — estate, gift, and income tax outcomes together — so the structure reflects the actual transfer, not just one piece of it.

Common Mistakes in Business Succession Planning

Waiting Too Long to Start

A 2023 University of Minnesota Extension survey of 286 businesses found the average owner was 59 years old, and only 21.6% had created or updated a written plan in the prior three years. Experts estimate family business transitions require 5 to 10 years to execute well — making delayed starts the most expensive mistake an owner can make.

Owners who start early can use gifting timelines, valuation strategies, and tax elections that simply aren't available in the final year before exit.

Three Other Mistakes That Derail Plans

- Choosing a successor on loyalty, not capability — the right owner and the right operator may be different people. Separating management succession from ownership succession is often the harder, more important conversation

- Treating the plan as a one-time document — business value, tax law, and family circumstances all change; the plan must change with them

- Skipping the professional team — succession planning spans accounting, tax, law, insurance, and financial planning. Only 34% of US family businesses have a robust, documented succession plan according to PwC — and most owners confuse "having a plan" with having one that's written and actionable

Relying on a single advisor — or no advisor at all — leaves gaps that no document can fix after the fact: missed tax elections, unenforceable agreements, and family disputes the plan was supposed to prevent.

Conclusion

A solid succession plan ties together leadership transition, ownership transfer, business valuation, legal structure, and tax and estate planning. Working through each area systematically ensures nothing gets overlooked when an actual transition is underway.

Starting early keeps the owner in control of the terms — who leads next, how ownership moves, what taxes apply, and what the family ultimately receives. Waiting tends to hand those decisions to circumstance rather than intention.

Frequently Asked Questions

What is the most common mistake in business succession planning?

Waiting too long to start. Owners who delay have fewer options for tax-efficient transfers, less time to develop successors, and inadequate legal protections in place when a triggering event actually occurs.

How early should I start succession planning for my business?

Most advisors recommend starting at least five to ten years before the intended exit. That lead time allows you to groom successors, execute gifting strategies, and align the plan with your estate and retirement goals.

What documents are needed for a business succession plan?

The core documents include:

- Buy-sell agreement

- Updated business entity operating or partnership agreement

- Revocable living trust (if applicable)

- Funded life insurance policies

- The succession plan document itself

What is a buy-sell agreement and why is it important?

A buy-sell agreement is a legally binding contract that determines what happens to an owner's interest when a triggering event — death, disability, or retirement — occurs. It shields both the departing owner's family and remaining owners from valuation disputes and loss of control.

How does business succession planning affect estate and gift taxes?

Transferring business interests without a plan can result in a large estate tax bill at the owner's death. Structured gifting, valuation discounts through FLPs or LLCs, and installment sales can significantly reduce this liability when planned well in advance.

What's the difference between management succession and ownership succession?

Management succession addresses who will run the business operationally. Ownership succession addresses who will hold the legal and financial interest. These may be different people, and a complete succession plan must address both separately.