Introduction

Transferring a family business to the next generation is one of the most consequential decisions an owner will ever make. Most owners approach it without a formal plan. The numbers are stark: according to the Conway Center for Family Business, only about 30% of family businesses survive to the second generation, 12% to the third, and just 3% beyond that.

Yet despite these odds, only 34% of family businesses globally have a documented succession plan, according to PwC's Global Family Business Survey.

This guide is for family business owners in the planning or pre-retirement stage who want a clear, practical framework for ownership transition — covering the full transfer of legal ownership, financial interests, and decision-making authority, not just a management handoff.

Following a structured 6-step process dramatically improves the odds that your business survives the transition intact.

Key Takeaways

- Family business ownership transition is a multi-year process that demands both financial planning and family alignment — it's far more than a legal handoff

- Communication breakdowns and unprepared heirs derail more transitions than financial problems ever do

- The 6 steps cover everything from valuing the business and preparing a successor to structuring the transfer and building long-term governance

- Starting 3–5 years before your intended exit gives you time to maximize value and prepare your successor properly

What Is Family Business Ownership Transition?

Family business ownership transition is the deliberate process of transferring legal ownership, management authority, and operational control from one generation or owner to a successor — whether a family member, a trusted employee, or an outside buyer.

It is not the same as day-to-day management succession. Handing someone the keys to run operations is a different act from transferring equity and economic rights. Ownership centers on dividend distributions, stock appreciation, and control. Management centers on growth, profitability, and innovation. Each requires its own timeline and documentation.

Family business transitions are complex because they sit at the intersection of:

- Personal relationships and generational expectations

- Wealth transfer and estate tax consequences

- Governance and legal structuring

- Family members who hold ownership stakes but don't work in the business

None of these layers exist in a standard third-party sale. That's why family businesses require a more deliberate, structured approach than most owners anticipate going in.

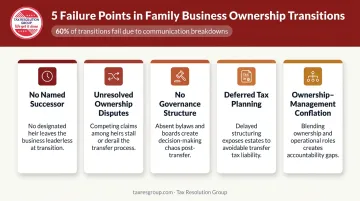

Why Family Business Transitions Often Fall Short

The central problem is not money. Research by Roy Williams and Victor Preisser found that 60% of family business transition failures stem from breakdowns in communication and trust, and 25% from inadequately prepared heirs. Only 15% are attributable to tax and legal failures.

That said, the financial and legal consequences of poor planning are severe enough to destroy an otherwise viable transition. Common failure points include:

- No named successor — owners delay the conversation until circumstances force a decision

- Unresolved ownership disputes — family members with different expectations about stakes and roles

- No governance structure — no clear decision-making authority after the transfer

- Deferred tax planning — missing opportunities to use lifetime gifting, installment structures, or trusts

- Ownership-management conflation — assuming that whoever runs the business should automatically own it

These patterns show up across the data. The Kreischer Miller Family Business Survey (2025) found that 45.9% of U.S. family-owned companies have no formal succession plan. The most cited barriers? Time constraints, emotional family dynamics, and a lack of clear direction — none of them informational.

The six steps below address each of these gaps directly, starting with the decisions most families delay the longest.

6 Steps for a Successful Family Business Ownership Transition

Step 1: Assess Your Business Value and Define Your Exit Goals

Before any transfer can be structured, you need clarity on two things: what the business is actually worth today, and what you want to achieve from the transition.

Your exit goals will shape everything that follows. Are you seeking maximum financial return? Preserving jobs for long-term employees? Keeping the business in the family regardless of price? There is no wrong answer, but an undefined answer makes every subsequent decision harder.

Start with a professional business valuation. The Exit Planning Institute reports that roughly 80% of business owners have never obtained a formal valuation. Without one, you cannot structure a sale, a gifting plan, or an estate strategy on realistic terms. Tax Resolution Group provides business valuation services that give owners an objective, data-backed picture of their company's worth — a necessary foundation before entering any transition process.

From there:

- Set an exit timeline — authoritative sources recommend beginning no later than 5 years out; complex transitions may need 10 or more

- Assemble your advisory team — at minimum, a CPA, an attorney, and a financial planner who have worked on business transitions before

- Align personal financial goals with business value — know what you need from the transfer to fund retirement or other objectives

Step 2: Separate Family Interests from Business Decisions

One of the most common — and most damaging — mistakes in family business transitions is letting personal relationships drive business decisions.

Placing an unqualified family member in leadership because they're the oldest child, or avoiding difficult ownership conversations to preserve the peace, almost always backfires. The business suffers, resentment builds, and the transition stalls or fails.

Establish explicit, written guidelines covering:

- Who is eligible for leadership roles and based on what criteria

- How compensation is determined for family members working in the business

- How ownership stakes are allocated among family members — including those not actively involved

- Who has final decision-making authority during the transition period

Just as critical: have the difficult conversations early and document them. Many families operate on unstated assumptions about who will take over. Those assumptions diverge. When they surface during a transfer — especially under the pressure of estate administration or tax deadlines — the conflict can be severe enough to unravel years of planning.

A structured family meeting, facilitated by a neutral advisor if needed, is often the most valuable step a family can take before any legal or financial work begins.

Step 3: Identify and Engage All Stakeholders

A family business transition affects more than the owner and the designated successor. Failing to communicate proactively with key stakeholders is one of the fastest ways to lose trust, talent, and client relationships during a transition.

Who counts as a stakeholder:

- Family members active in the business

- Family members with ownership stakes but no operational role

- Long-tenured employees, particularly those in senior or client-facing roles

- Key customers whose relationships may be tied to the current owner personally

- Vendors and partners with long-standing contracts

Each group has distinct concerns. Senior employees worry about job security and reporting structure. Key customers worry about whether service quality will hold. Family members outside the business worry about their financial interests being protected.

Early, transparent communication — through regular family meetings, employee briefings, and where appropriate, direct outreach to key clients — reduces the anxiety that drives talent and customers to look elsewhere. The longer people operate without clear answers, the more likely they are to make their own plans.

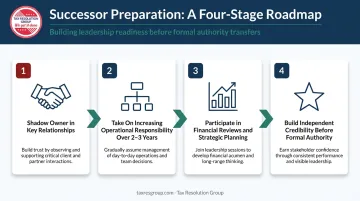

Step 4: Select and Prepare Your Successor

Identifying the right successor is one of the highest-stakes decisions in the entire process. The right choice comes down to capability, commitment, and credibility — not birth order or family expectation.

That successor may be a family member, a trusted senior employee, or an outside hire. According to PwC's 2023 Global Family Business Survey, 71% of family businesses intend to keep ownership in the family. But intention and readiness are different things: Conway Center data shows fewer than half of owners planning to retire within five years have actually selected a successor.

Successor preparation should be gradual and structured:

- Shadow the current owner in key client and vendor relationships

- Take on increasing operational responsibility over 2–3 years

- Participate in financial reviews and strategic planning early

- Build independent credibility with employees before assuming formal authority

Only 39% of family businesses have a formal development plan for future leaders, per Kreischer Miller's 2025 survey. The remaining 61% rely on ad hoc approaches that often leave successors underprepared — a direct contributor to transition failure.

The outgoing owner's willingness to genuinely transfer knowledge — including the cultural and relational dimensions of the business, not just the operational mechanics — is as important as any formal training program.

Step 5: Structure the Legal and Financial Transfer

Once you know who is taking over and what the business is worth, the next decision is how ownership actually transfers. Each mechanism carries different implications for control, timing, tax exposure, and the financial interests of uninvolved family members.

Common ownership transfer mechanisms:

| Method | Best For | Key Tax Consideration |

|---|---|---|

| Outright sale (cash) | Clean exit, third-party buyers | Capital gains tax on appreciation above basis |

| Installment sale | Family buyers with limited liquidity | Gain spread over payment period, reducing annual tax impact |

| Lifetime gifting | Gradual transfer over time | Subject to annual exclusion ($19,000/recipient in 2026) and lifetime exemption ($15M in 2026) |

| GRAT (Grantor Retained Annuity Trust) | Minimizing taxable gift value | No gain on transfer into trust; taxable gift reduced by present value of retained annuity |

| Hybrid approach | Mixed goals | Combines benefits and complexity of multiple methods |

The stakes of getting this wrong are real. Estate taxes can reach 40% on taxable estate value above the basic exclusion — meaning a business valued above the exemption threshold that hasn't been properly structured for transfer can trigger a forced liquidation to cover the tax bill.

Tax Resolution Group's tax consulting services help family business owners evaluate transfer structures, model tax outcomes, and avoid the costly missteps that come from structuring a transfer without proper advisory support.

Legal documentation matters equally. Before any transfer is finalized, ensure the following are current and properly drafted:

- Buy-sell agreement

- Shareholder or operating agreement updates

- Estate planning documents reflecting the new ownership structure

Step 6: Build a Governance Structure and an Agile Succession Plan

Ownership transfer is not the finish line. Without a clear governance framework in place, new leadership often faces immediate authority disputes, unclear decision-making protocols, and family members reopening ownership questions that were supposedly settled.

A governance structure should define:

- Who holds decision-making authority and for what categories of decisions

- How disputes are resolved — whether through a family council, board of advisors, or external mediator

- Roles and boundaries for family members who hold ownership but don't work in the business

- Communication cadence for ownership-level updates and financial reporting

The succession plan itself must also be treated as a living document, not a one-time exercise. Business conditions change. Tax laws change — the "One Big Beautiful Bill" recently made elevated estate tax exclusions permanent, altering the planning calculus significantly. Family dynamics evolve. A plan that isn't reviewed periodically becomes outdated and unreliable precisely when it's needed most.

Schedule an annual review of the succession plan with your advisory team. Update it when any of the following change: business valuation, tax law, family circumstances, or the successor's readiness or interest.

Common Mistakes to Avoid When Transitioning a Family Business

Waiting Too Long to Start

Many owners delay until illness, burnout, or an unexpected acquisition offer forces the issue. At that point, options narrow dramatically. Beginning 3–5 years out — and ideally earlier — gives you time to maximize business value, structure the transfer tax-efficiently, and prepare the successor without rushing.

Confusing Management Transition with Ownership Transition

Handing someone operational control is not the same as transferring legal ownership. Both require separate documentation, timelines, and decisions. Conflating them leads to ambiguity about who actually holds financial authority and liability — a particularly dangerous gap when estate or tax questions arise.

Overlooking the Tax and Legal Complexity

That legal ambiguity compounds quickly when tax exposure enters the picture. Without proper planning, estate taxes can consume up to 40% of the taxable business value above the exclusion threshold. Families that skip common mitigation strategies leave significant, avoidable money on the table. Those strategies include:

- Annual gifting exclusions to gradually shift ownership with minimal tax impact

- Installment sale structures that spread the tax burden over time

- Trust-based arrangements that protect assets and reduce estate value

IRS scrutiny on business valuations has also intensified, backed by $80 billion in new enforcement funding. Poor documentation raises the cost of an audit considerably. A CPA with succession planning experience can help structure the transfer correctly from the start.

Frequently Asked Questions

What is the best way to transfer family business ownership to a family member?

The best method depends on your goals. Options include gifting shares over time, a family installment sale, or a hybrid structure combining both. Each carries distinct tax and legal implications, so working with a CPA and an attorney before committing to a structure is essential.

What are the ownership stages in a family business?

The standard framework (Gersick et al., 1997) identifies three: the Controlling Owner stage, the Sibling Partnership stage, and the Cousin Consortium stage. Each comes with distinct governance challenges and succession dynamics as ownership spreads across generations.

What are the 5 D's of family business succession planning?

The 5 D's — Death, Disability, Divorce, Disagreement, and Distress — represent the unplanned triggers that force rushed transitions. A documented succession plan — completed before any of these events — is the most effective defense.

What is the three-generation rule in family business?

The adage "shirtsleeves to shirtsleeves in three generations" describes the pattern where the first generation builds wealth, the second preserves it, and the third depletes it. Research has documented a 70% failure rate in wealth transfers across generations — intentional planning and governance structures are the primary antidote.

How long does a family business ownership transition take?

A well-planned transition typically takes 3–5 years from initial planning to final transfer. Transitions completed in under a year are far more likely to result in unresolved conflict, missed tax opportunities, or business disruption.

What are the tax implications of transferring a family business to a family member?

Tax implications vary by transfer method:

- Sales may trigger capital gains tax on any appreciation

- Gifts are subject to the annual exclusion ($19,000 per recipient in 2026) and the lifetime exemption ($15 million in 2026)

- Estate transfers face their own thresholds and a maximum rate of 40%

Work with a CPA before finalizing any transfer structure.