: Complete Guide](https://file-host.link/website/taxresgroup-er1vd1/assets/blog-images/bfafe632-bcc0-45fd-b685-5cf2259f7bfc/1783034488500870_f0da523e44d8463dbdb4708d5000f87e/360.webp)

Introduction

Most small business owners know the feeling: it's March, tax deadlines are closing in, and the books are a mess. Receipts are scattered, bank accounts haven't been reconciled in months, and nobody's sure which expenses are actually deductible. That scramble is preventable — and virtual bookkeeping is how most businesses prevent it.

Virtual bookkeeping delivers professional recordkeeping remotely, keeping your financials current every month rather than forcing a chaotic year-end catch-up. Paired with tax preparation — through the same firm or a coordinated workflow — it creates a system where clean books feed directly into accurate, defensible tax returns.

This guide covers:

- What virtual bookkeeping and tax preparation actually include

- How the process works month to month

- How clean books support tax compliance year-round

- What it costs compared to hiring in-house

- Which tax mistakes it prevents — and what those mistakes cost

- How to choose the right provider

The points below summarize what you'll take away from each section.

Key Takeaways:

- Virtual bookkeeping is professional recordkeeping delivered remotely via cloud software

- Clean monthly books are the foundation for accurate quarterly estimated tax payments

- The IRS underpayment penalty rate is 7% for individuals; accuracy-related penalties hit 20% of underpaid tax

- In-house bookkeeping runs ~$70,400/year fully loaded; virtual services typically cost $2,388–$7,188/year

- Tax Resolution Group provides bookkeeping and tax preparation as integrated services, eliminating handoff errors

What Is Virtual Bookkeeping and Tax Preparation?

Virtual bookkeeping is professional bookkeeping performed remotely — using cloud accounting software, bank feeds, and secure document platforms instead of a desk down the hall. The tasks are identical to what an in-house bookkeeper would do:

- Recording and categorizing transactions

- Reconciling bank and credit card accounts

- Managing accounts payable and receivable

- Generating monthly financial reports

The "virtual" part refers to delivery method, not service quality.

Combined Service vs. Coordinated Workflow

When people talk about "virtual bookkeeping and tax preparation," they usually mean one of two things:

- Single-provider model — one firm handles both functions. The bookkeeper maintains the records; the tax professional uses those same records to prepare and file returns. There's no gap between the two.

- Split-provider model — a virtual bookkeeper maintains records and delivers an organized financial package to a separate tax preparer at year-end.

The distinction matters. With a combined provider, the handoff is internal — no time wasted reformatting data or explaining categorization choices. With separate providers, you're responsible for making sure your bookkeeper and tax preparer are aligned.

Bookkeeping vs. CPA Services: The Scope Boundary

These are different roles, and understanding where one ends helps clarify what the other provides. A bookkeeper maintains records and produces reports. A CPA or Enrolled Agent handles tax strategy, prepares and files returns, provides compliance guidance, and can represent you before the IRS.

Neither replaces the other — accurate books make tax work faster and more defensible; tax strategy, in turn, shapes how transactions get categorized throughout the year. Tax Resolution Group combines both functions under one roof, so the records your bookkeeper maintains feed directly into your tax preparation without reformatting, reclassification, or back-and-forth between separate firms.

How Virtual Bookkeeping Works: The Process

Onboarding and Access

A virtual bookkeeper needs access to your financial data, not your office. Setup typically involves:

- Bank and credit card feeds — permissioned read-only data access so transactions flow automatically into the accounting software

- Accounting platform access — most commonly QuickBooks Online, where the bookkeeper works directly in your books

- Document storage — a secure portal for uploading receipts, invoices, and prior-year statements

There are no physical document handoffs or sensitive files sent over email. Tax Resolution Group uses QuickBooks as its primary shared accounting solution, giving clients direct access to upload information and see their financials in real time.

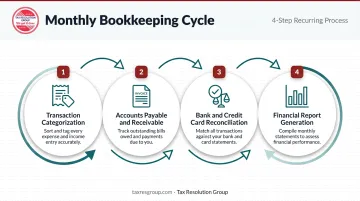

The Monthly Workflow

Each month, a virtual bookkeeper runs through a consistent cycle:

- Transaction categorization — incoming bank feed transactions are reviewed, categorized, and coded to the correct accounts

- Accounts payable and receivable — invoices tracked, payments recorded, aging reports maintained

- **Bank and credit card reconciliation** — every account balanced against statements

- Financial report generation — profit & loss statement, balance sheet, and cash flow statement delivered to the client

When this cycle runs every month without gaps, tax season becomes a matter of reviewing clean records — not reconstructing a year's worth of transactions under deadline pressure.

Security Protocols

Remote financial services raise real security questions. The IRS requires tax and accounting practices to maintain a Written Information Security Plan under GLBA/FTC Safeguards rules, and compliance is mandatory. Qualified virtual bookkeeping providers implement:

- Encrypted data storage and secure connections

- Login protection and account activity alerts

- Multi-factor authentication

- Third-party vendor accountability through written agreements

Tax Resolution Group maintains a dedicated security team, encrypts files at rest, blocks repeated login attempts, and restricts third-party data access to tasks performed on the firm's behalf.

What You're Responsible For

Security and compliance sit with the provider. Day-to-day recordkeeping does too — but the bookkeeper can only work with what you give them. Your responsibilities include:

- Categorizing any unusual or ambiguous transactions when asked

- Providing receipts and documentation for deductions

- Communicating changes in business activity (new revenue streams, major purchases, payroll changes)

How Virtual Bookkeeping Supports Tax Preparation Year-Round

Why Monthly Books Matter for Taxes

Tax compliance isn't a once-a-year event — it's the result of accurate work performed every month. When books are reconciled monthly, the year-end close becomes a straightforward process rather than a frantic scramble to reconstruct months of missing data.

Current books also reduce audit risk. The IRS can disallow deductions without supporting documentation, and IRS Publication 583 is explicit: businesses must keep records for income, expenses, assets, and employment taxes. A virtual bookkeeper keeps that documentation organized throughout the year, so nothing is missing if the IRS comes asking.

Quarterly Estimated Taxes

Those monthly records also have a direct cash impact at the quarterly level. According to the IRS, sole proprietors, partners, and S corporation shareholders generally must make estimated tax payments if they expect to owe $1,000 or more when filing; corporations use a $500 threshold.

Without current books, most business owners are guessing at their quarterly liability. That guess is often wrong. For the quarter beginning July 1, 2026, the IRS underpayment rate is 7%, applied to every dollar underpaid and every quarter it remains underpaid. Accurate monthly records make correct estimates possible before the deadline, not after.

The Year-End Tax Handoff

By January or February, a virtual bookkeeper should be able to deliver a complete financial package to the tax preparer, including:

- Year-end profit and loss statement

- Balance sheet

- Payroll summary

- Accounts receivable/payable aging reports

- Fixed asset schedule

- Bank reconciliation reports

- Documentation supporting major deductions

When bookkeeping and tax preparation happen within the same firm — as they do at Tax Resolution Group — this handoff is internal. The tax preparer already knows the books, the categorization logic, and the client's business. There's no catch-up meeting, no reformatting, and no risk of miscommunication between two unrelated professionals.

Key Benefits of Virtual Bookkeeping for Small Businesses

Cost Savings

The cost difference between virtual bookkeeping and an in-house hire is significant. According to the Bureau of Labor Statistics Occupational Outlook Handbook, the May 2024 median annual wage for bookkeeping, accounting, and auditing clerks was $49,210. Adding benefits using BLS March 2026 employer compensation data — where wages represent 69.9% of total compensation — puts the fully loaded cost of an in-house bookkeeper at roughly $70,400/year.

Published virtual bookkeeping pricing runs considerably lower:

| Service Tier | Monthly Fee | Annual Cost |

|---|---|---|

| Entry-level (e.g., Bench Grow) | ~$199/month | ~$2,388 |

| Mid-tier (e.g., Bench Core) | ~$399/month | ~$4,788 |

| Full-service with tax (e.g., Bench Core + Tax) | ~$599/month | ~$7,188 |

| Estimated in-house bookkeeper | — | ~$70,400 |

Tax Resolution Group positions its pricing as a fraction of a full-time employee's cost, with tiered plans available upon consultation.

Scalability and Expertise

Virtual bookkeeping scales with your business. A seasonal business can adjust service scope without hiring delays or severance costs. A growing startup can add complexity — payroll, multi-entity, accrual accounting — without recruiting a more senior hire.

That flexibility extends to expertise. Virtual bookkeeping firms stay current on software changes, regulatory updates, and platform integrations — so you don't have to. Tax Resolution Group's QuickBooks Certified ProAdvisors cover:

- Software setup and configuration for QuickBooks Online and QuickBooks Desktop

- Staff training so your team uses the platform correctly from day one

- Ongoing support and troubleshooting as your business evolves

- Clean-up engagements to correct historical errors before tax season

Accurate, well-maintained books don't just simplify filing — they give you reliable data for decisions, audit defense, and strategic planning.

Tax Mistakes Virtual Bookkeeping Prevents

Misclassified Expenses and Commingled Accounts

Personal expenses logged as business deductions, costs coded to the wrong category, owner draws mixed with operating expenses — these create two problems. First, they misstate your actual tax liability. Second, they create accuracy-related penalty exposure: the IRS charges 20% of the underpayment attributable to negligence or substantial understatement.

Professional bookkeeping applies consistent categorization standards every month. Misclassifications get caught before they become return errors, not after an audit. That distinction — caught in the books versus caught in an audit — is where the real cost difference lives.

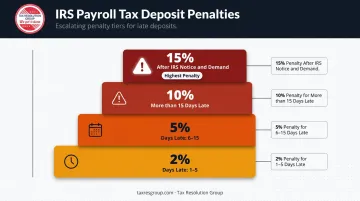

Missing Quarterly Payments and Payroll Errors

Underpaid quarterly estimates cost 7% annually. But payroll tax deposit errors carry a tiered penalty structure that escalates quickly:

- 2% — 1 to 5 days late

- 5% — 6 to 15 days late

- 10% — more than 15 days late

- 15% — after IRS notice and demand

These penalties are automatic. They don't require an audit trigger — just a missed deposit. A virtual bookkeeper tracks payroll obligations and keeps calendars current, so a missed deposit date doesn't turn into a compounding penalty that dwarfs the original amount owed.

How to Choose the Right Virtual Bookkeeper or Firm

Credentials and Scope

Look for providers who clearly state what's included — and what's not. Key credentials to look for:

- QuickBooks ProAdvisor — confirms platform expertise for the day-to-day books

- Enrolled Agent (EA) — the highest credential the IRS awards; critical if the firm handles tax notices, audits, or collections

- CPA — necessary for tax strategy, complex filings, and any regulated assurance work

A firm that offers bookkeeping without any licensed tax professional on staff can't help when your return is questioned. A firm with both can.

Industry Experience and Software Fit

A bookkeeper familiar with your industry understands your expense categories, typical cost structures, and compliance requirements. Tax Resolution Group, for example, works across media and entertainment (pre/post-production accounting, payroll), construction (job costing, QuickBooks Online setup), and professional services — where each vertical carries different compliance demands and cost structures.

That industry depth matters because transactions don't exist in isolation. A bookkeeper who knows your sector can flag anomalies, apply the right expense categories, and give you numbers that actually reflect how your business works.

Communication and Data Security

Even with the right credentials and industry fit, a poor communication setup creates friction fast. Before signing, evaluate:

- Communication format — video calls, portal messages, email updates, or a mix?

- Access to your own data — can you log in and see current financials at any time?

- Security documentation — can they explain their data protection practices in plain terms?

Avoid any provider who cannot clearly describe how your data is protected. IRS Publication 5708 makes a written information security plan a requirement, not a differentiator.

Frequently Asked Questions

Is virtual bookkeeping legitimate?

Yes. Virtual bookkeeping is a widely used professional service delivered by credentialed accountants and bookkeepers using the same cloud platforms — QuickBooks, Xero — used by major accounting firms. Reputable providers operate under IRS security requirements and professional standards.

Do virtual bookkeepers work with tax preparers?

Yes. Virtual bookkeepers regularly deliver organized financial packages — P&L statements, reconciliation reports, payroll summaries — to tax preparers for filing. Some firms, including Tax Resolution Group, handle both functions in-house, which eliminates the coordination gap between separate providers.

What is the difference between a virtual bookkeeper and a CPA?

A bookkeeper maintains financial records and produces reports. A CPA provides tax strategy, prepares and files returns, and offers compliance guidance. Both roles are needed — bookkeepers keep the records accurate; CPAs use those records to minimize tax liability and ensure compliance.

Can virtual bookkeeping help with quarterly estimated taxes?

Yes. Correct quarterly estimated tax payments require knowing your current taxable income. Without up-to-date books, business owners are guessing — and guessing wrong triggers IRS underpayment penalties on the shortfall.

How much does virtual bookkeeping typically cost?

Most virtual bookkeeping tiers run $199–$599/month, compared to an estimated $70,400/year for a fully loaded in-house bookkeeper (BLS wage and benefits data). First-year costs may also include a one-time onboarding or catch-up fee.

What records should I give my virtual bookkeeper access to?

The core access needed includes:

- Bank and credit card feeds (read-only)

- Accounting software login

- Payroll records

- Receipts and invoices via a secure document platform

- Prior-year financial statements or tax returns for context