Introduction

Picture this: a business owner spends 25 years building a thriving company — great clients, loyal employees, real revenue. Then a health scare hits. Suddenly, there's no plan, no documented processes, and no clear answer to "what happens now?" The business that represents most of their net worth hangs in the balance.

This isn't a rare edge case. Gallup's 2024 survey found that one-third of business owners had no long-term plan or were unsure about their business's future — the same uncertainty that turns a health scare or sudden departure into a financial crisis.

Succession planning is a risk management strategy — one every small business owner needs, regardless of when they plan to exit.

This guide covers:

- What succession planning actually means for small businesses

- Why skipping it is financially dangerous

- The main transition options available

- A step-by-step process to build your plan

- Key tax and valuation considerations

What Is Business Succession Planning?

Business succession planning is the process of deciding — in advance — who will take over your business, how ownership will transfer, and when. It applies to any ownership change: retirement, disability, death, partnership disputes, or deciding it's time to move on.

For small business owners, a complete succession plan typically addresses:

- Successor identification — who takes over leadership and ownership

- Transfer mechanism — whether ownership is sold, gifted, or transitioned gradually

- Legal agreements — buy-sell agreements, partnership agreements, or estate documents

- Financial alignment — ensuring the transition funds your retirement or other personal goals

One distinction worth getting right early: a succession plan is not the same as a will. A will governs what happens to your assets after death. A succession plan governs what happens to your operating business — which requires a different set of decisions, documents, and timelines altogether.

Why Small Business Owners Can't Afford to Skip Succession Planning

The Numbers Are Stark

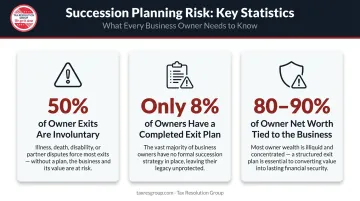

A 2022 MassMutual study of small and mid-sized business owners found that only 8% had completed an exit plan, and only 32% had a buy-sell agreement in place. Of those with agreements, 47% hadn't reviewed them in more than three years.

Meanwhile, the Exit Planning Institute reports that roughly 50% of owner exits are involuntary — triggered by death, disability, divorce, distress, or disagreement. No warning. No runway. No favorable negotiating position.

The Financial Consequences Are Real

Without a plan, business value erodes fast during a chaotic transition. Consider what happens when an unplanned exit forces a rushed sale:

- Buyers and lenders discount businesses that depend heavily on one person

- Clean financials and documented processes — which buyers require — haven't been built

- Employees and customers may leave before a deal closes

- Only 20% to 30% of businesses that go to market actually sell, according to the Exit Planning Institute

Your Retirement Is Tied to This Business

For most small business owners, 80% to 90% of their net worth is tied up in the business itself — not in savings accounts, pensions, or investment portfolios. That concentration makes succession planning less of an estate concern and more of a retirement strategy.

A chaotic, unplanned exit doesn't just disrupt operations. It compresses timelines, shrinks buyer pools, and forces price concessions at exactly the moment owners need maximum value. Getting ahead of that outcome is what succession planning is built to do.

Your Succession Options: Which Path Is Right for You?

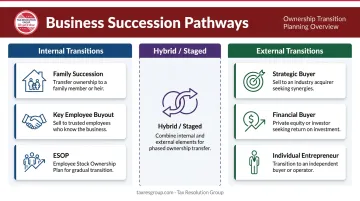

The right succession path depends on your goals, your business's financial health, and who can realistically take over. Options generally fall into two categories: internal transitions and external sales.

Internal Succession Options

Family succession is the most emotionally complex option. Passing ownership to a child or family member requires planning around estate equalization, gift tax implications, and genuinely preparing the next generation to lead. According to the Cornell SC Johnson College of Business, only about 40% of U.S. family businesses successfully transition to the second generation, and roughly 13% reach the third. Test successor readiness early — and keep a backup plan.

Management or key employee buyout involves an existing employee or leadership team purchasing the business — typically through a buy-sell agreement funded via seller financing or third-party lending. This path preserves continuity and culture, but the employee needs either personal financing or a seller-financed arrangement they can realistically service.

Employee Stock Ownership Plans (ESOPs) allow employees to gradually acquire ownership through a company-funded trust. The NCEO reports there are currently 6,098 privately held ESOP companies in the U.S. ESOPs work for smaller businesses, but they require specialized legal and tax structuring — expect to work with an attorney and a CPA experienced in ESOP transactions.

External Succession Options

Sale to an outside buyer often commands higher valuations, but demands real preparation. Buyers typically fall into three categories:

- Strategic buyers — competitors or suppliers acquiring for market position

- Financial buyers — private equity firms focused on returns

- Individual entrepreneurs — owner-operators buying a running business

All three expect clean financials, documented processes, and a business that doesn't rely on the owner to function.

Hybrid or staged transitions offer a middle path for owners who aren't ready for a clean break. Bringing in a minority partner, phasing out operational responsibilities over two to three years, or tying an exit to revenue milestones all reduce transition risk — and give a successor time to earn credibility before assuming full control.

How to Build a Business Succession Plan: Step by Step

Step 1 — Define Your Goals and Timeline

Before anything else, answer these questions:

- What do you want from this transition — maximum payout, legacy preservation, employee protection, or family continuity?

- When do you want to exit, and how involved do you want to remain afterward?

SBDCNet's 2024 succession planning guide recommends identifying leadership needs and business changes within a one-to-five-year lead time. For family transitions, the Family Business Association recommends starting 10 to 15 years before your target retirement date.

Step 2 — Identify and Evaluate Your Successor

Who is realistically capable and willing to take over? This single decision shapes everything else: how the transfer is funded, how it's structured legally, and how long you need to prepare. Run an honest assessment. Emotional attachment to a family member or loyal employee doesn't substitute for readiness.

Step 3 — Assemble Your Advisory Team

Succession planning is not a solo process. A functional advisory team typically includes:

- A CPA or accountant — for tax structuring, financial analysis, and business valuation

- A business attorney — for drafting buy-sell agreements and legal transfer documents

- A business valuation professional — to establish what the business is actually worth

Tax Resolution Group works with small businesses on the tax structuring, financial modeling, and business valuation components of this process — helping owners understand what they'll actually keep from the transition after taxes and fees.

Step 4 — Get a Business Valuation

You can't plan a transfer without knowing the starting value. A professional valuation sets realistic expectations, informs buy-sell agreement terms, and tells you whether the business's current value meets your retirement goals — or whether you need to build value before exiting.

MassMutual found that only 20% of business owners had obtained a valuation specifically to fund a buy-sell agreement, while 61% said knowing their business value was important. That gap — between knowing it matters and actually doing it — is where most succession plans fall apart.

Step 5 — Draft the Legal Framework

The core document in most small business succession plans is the buy-sell agreement. It defines:

- Triggering events — death, disability, retirement, disagreement, or departure

- Valuation method — how the business will be priced at the time of transfer

- Payment terms — lump sum, installment, or insurance proceeds

This document needs to be in writing even for family transitions. Verbal agreements don't hold up legally when circumstances change.

Step 6 — Fund the Transition and Review Regularly

Common funding mechanisms include:

- Life insurance on key owners (used by 46% of owners with buy-sell agreements, per MassMutual)

- Installment notes from the buyer

- Sinking funds built up over time

Review the plan every two to three years. Business value changes. Successors change. Goals change. A plan written five years ago with no updates is likely out of step with your current business and personal circumstances.

The Role of Valuation and Tax Planning in Succession

Why Valuation Comes First

An accurate business valuation is the foundation of every succession plan. It determines the sale price, informs legal agreements, and reveals whether the business is ready for transition or needs improvement first.

Many small business owners significantly overestimate or underestimate their value without an objective third-party assessment — and BizBuySell's broker surveys have repeatedly found that unrealistic asking prices are the top reason deals fall apart.

A qualified CPA or valuation specialist can provide that third-party perspective — grounding the number in historical financials and current market conditions rather than owner assumptions. Tax Resolution Group's business valuation services are designed specifically for this purpose, giving owners a defensible starting point before any succession decisions are made.

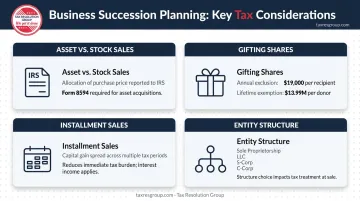

Major Tax Considerations

Tax decisions in a succession are not one-size-fits-all. The key variables include:

- Asset sales vs. stock sales — Per IRS Publication 544, selling a business is generally treated as selling each asset separately, and each asset's gain or loss character can differ significantly. Form 8594 may be required for both buyer and seller.

- Gifting shares to family members — The 2025 annual gift tax exclusion is $19,000 per donee, with a lifetime exemption of approximately $13,990,000. These figures are subject to change — the post-2025 legislative landscape around the TCJA sunset could significantly reduce the lifetime exemption, which is exactly why current tax counsel matters.

- Installment sales — Per IRS Publication 537, installment sales spread gain recognition across payment periods. Some assets, like inventory, may not qualify for the same installment treatment.

- Entity structure — Whether the business is a sole proprietorship, LLC, S-corp, or C-corp affects how any transfer is taxed. Restructuring before a sale is sometimes worth considering — but only with proper modeling.

These decisions should be modeled with a CPA well before any transaction is executed. The differences in after-tax proceeds between structures can be substantial.

Common Mistakes Small Business Owners Make

Waiting too long to start. Most owners underestimate how long it takes to prepare. Building leadership depth, cleaning up financials, and identifying a qualified successor can each take years on their own. For most owners, urgency arrives only after a health crisis or a forced sale — by then, it's too late to plan well.

Failing to document operations. A business that only runs because the owner holds all the knowledge in their head is extremely difficult to transfer. Buyers and successors need documented systems, clear role definitions, and accessible customer relationship information. A business that runs without its owner commands a higher valuation.

Treating the plan as a one-time document. Once documentation is in place, the work isn't done. A succession plan isn't a box to check once and file away. Business value changes. Tax laws change. Successors change. The plan needs regular review — at minimum every two to three years — to remain relevant and enforceable.

Frequently Asked Questions

What is a succession plan for a business?

A business succession plan is a documented strategy that defines who will take over ownership and leadership, how ownership will transfer, and when — covering businesses of all sizes and any type of ownership change, not just retirement.

When should a small business owner start succession planning?

Most advisors recommend beginning at least three to five years before your target transition date. For family succession, starting 10 to 15 years out gives you time to build business value, prepare a successor, and optimize tax structure.

What are the main types of business succession for small businesses?

The core options are transferring to a family member, selling to a key employee or management team, and selling to an outside buyer. Hybrid approaches — such as bringing in a minority partner first or phasing out gradually — are also common and often reduce transition risk.

What happens if a small business owner dies without a succession plan?

The business may be forced into a chaotic or deeply discounted sale. The estate can face legal complications determining ownership, and employees and customers may leave before any deal closes. The resulting transition is typically far more costly and damaging than a planned one.

How is a small business valued for succession planning purposes?

A professional valuation examines earnings (typically measured using EBITDA), revenue consistency, asset values, and comparable business sales. Working with a qualified accountant or business valuation professional is strongly recommended, as self-assessed values are frequently off by a significant margin in either direction.

Do I need an attorney and accountant for business succession planning?

Both are typically essential. An attorney drafts the legal agreements, particularly the buy-sell agreement. A CPA handles the tax structuring, financial analysis, and valuation components that determine what the owner actually nets from the transition. Neither role substitutes for the other.