For small business owners, HR managers, and growing companies, getting payroll right isn't optional. The IRS assessed over $1.15 billion in employment-tax civil penalties in FY 2025 alone, with more than 4.4 million individual assessments. Those numbers reflect what happens when payroll goes wrong — missed deposits, misclassified workers, late filings.

This guide walks through exactly how payroll works, what the law requires, and how to choose the right approach for your business.

Key Takeaways

- Payroll processing covers gross wage calculation, tax withholding, payment disbursement, and tax filing — far more than simply issuing checks

- The process follows three stages: pre-payroll setup, active calculation, and post-payroll compliance

- Federal laws (FLSA, FICA, FUTA) set non-negotiable minimum requirements for every employer

- Manual, software, outsourced, and managed payroll each carry different trade-offs across cost, accuracy, and compliance exposure

What Is Payroll Processing?

Payroll processing is the recurring business function that calculates employee earnings, applies required deductions, and delivers net pay — typically on a weekly, biweekly, semimonthly, or monthly schedule. According to BLS data from 2023, biweekly is the most common pay frequency among U.S. private employers at 43.0%, followed by weekly at 27.0%, semimonthly at 19.8%, and monthly at 10.3%.

Three terms frequently get used interchangeably, but they refer to distinct functions:

- Payroll — the total compensation owed to employees

- Payroll processing — the operational system that executes payment, including calculation, withholding, disbursement, and filing

- Payroll accounting — the separate function of recording payroll transactions in the general ledger

The IRS frames employer payroll obligations around four core duties: withholding federal income tax, withholding and matching Social Security and Medicare taxes, depositing employment taxes electronically, and filing employment tax returns. That framing cuts to the heart of what payroll actually is: a compliance function with a payment component, not simply a disbursement system with some tax rules attached.

How the Payroll Process Works: A Step-by-Step Breakdown

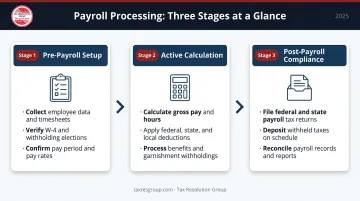

Payroll processing follows three stages: pre-payroll setup, active calculation, and post-payroll compliance. Each must be completed in sequence — errors carry forward.

Step 1: Collect and Verify Employee Data

Before any calculation starts, gather and validate:

- Employee classification (hourly vs. salaried)

- Hours worked during the pay period

- Current pay rates

- W-4 withholding elections (IRS Publication 15 requires employers to collect a signed W-4 from every new hire before the first wage payment)

- Benefits elections and any changes from the prior period

When an employee submits a new W-4, the employer must implement it no later than the first payroll period ending on or after the 30th day from receipt. Missing that window creates a withholding error that can compound across multiple pay periods.

Step 2: Calculate Gross Pay

Gross pay calculation differs by worker type:

- Hourly workers: Hours worked × hourly rate

- Salaried workers: Annual salary ÷ number of pay periods

Add any overtime, bonuses, commissions, and PTO payouts on top of base pay. Under the Fair Labor Standards Act, covered nonexempt employees must receive overtime at 1.5× their regular rate for all hours worked beyond 40 in a workweek. The federal minimum wage floor is $7.25/hour, though many states set higher rates.

Step 3: Apply Deductions and Withholdings

Deductions fall into two categories:

Mandatory deductions:

- Federal and state income tax (based on W-4 elections and applicable tax tables)

- FICA contributions — 6.2% Social Security (up to the $184,500 wage base in 2026) and 1.45% Medicare, both from the employee's wages

- Wage garnishments ordered by a court or agency

Voluntary deductions:

- Health insurance premiums

- 401(k) or other retirement contributions

- FSA/HSA contributions

Gross pay minus total deductions equals net pay — the amount the employee actually receives.

Step 4: Disburse Payment and Issue Pay Stubs

Common payment methods include direct deposit, paper check, and pay cards. Most states legally require employers to provide a pay stub showing gross pay, each deduction, and net pay.

Direct deposit processes through the ACH network. Per Nacha, ACH payments can settle same day, next day, or within two business days — ACH deposits typically clear by 9 a.m. on payday.

Step 5: File Payroll Taxes and Maintain Records

Post-payroll obligations are where many businesses fall short. Missing these deadlines triggers penalties, so track them carefully:

| Filing | Deadline |

|---|---|

| Federal tax deposits | Per IRS deposit schedule, via EFTPS |

| Form 941 (quarterly) | Last day of the month following quarter-end |

| Form 940 (annual FUTA) | January 31 (or February 10 if all FUTA tax deposited on time) |

Recordkeeping requirements under DOL Fact Sheet #21:

- Payroll records: at least 3 years

- Time records (time cards, wage-rate tables, work schedules): at least 2 years

Payroll Compliance and Regulatory Requirements

Payroll compliance isn't a single law — it's a stack of overlapping federal and state requirements.

FLSA: Wages, Overtime, and Records

The Fair Labor Standards Act sets the federal minimum wage at $7.25/hour and mandates overtime at 1.5× the regular rate after 40 hours. It also establishes mandatory recordkeeping requirements. The biggest risk here is misclassifying employees as overtime-exempt when they don't meet the legal criteria — that creates retroactive back-pay liability plus penalties.

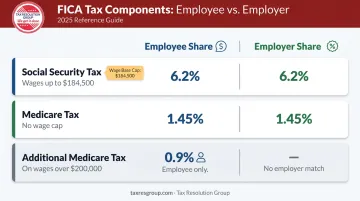

FICA: Social Security and Medicare

Both employees and employers each contribute:

- Social Security: 6.2% on wages up to $184,500 (2026 wage base)

- Medicare: 1.45% with no wage base cap

- Additional Medicare Tax: Employers must withhold an extra 0.9% on employee wages exceeding $200,000 in a calendar year — there's no employer match on this portion

FUTA: Federal Unemployment Tax

FUTA applies solely to the employer ; nothing is withheld from employee wages. The standard rate is 6.0% on the first $7,000 of each employee's annual wages. Employers that pay state unemployment taxes (SUTA) on time can claim a credit of up to 5.4%, reducing the effective federal rate to 0.6%. SUTA rates and wage bases vary by state and change annually.

State-Level Obligations

Each state adds its own layer of requirements on top of federal rules:

- Income tax withholding rates and thresholds

- State minimum wage floors (often higher than the federal $7.25)

- Pay frequency mandates (weekly, bi-weekly, or semi-monthly)

- Recordkeeping and notice requirements

Multi-state employers face compounding complexity. A business with employees in California, Texas, and New York tracks three separate rule sets simultaneously — each with its own filing deadlines, wage bases, and penalty structures. This is consistently one of the highest-risk areas for compliance gaps.

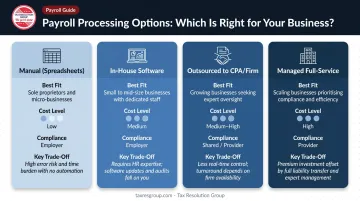

Types of Payroll Processing: Choosing the Right Approach

The right payroll approach depends on your company size, internal expertise, and workforce complexity. What works for a solo operator rarely holds up for a growing team with multi-state employees.

The Four Main Options

| Approach | Best For | Key Trade-Off |

|---|---|---|

| Manual (spreadsheets) | Solo operators, very early-stage | Low cost, but highly error-prone and time-consuming |

| In-house payroll software | Small teams with a knowledgeable admin | Efficient, but compliance still falls on you |

| Outsourced to a CPA/payroll firm | Growing businesses, complex structures | Shifts compliance burden; deep tax expertise |

| Managed/full-service payroll | Larger businesses, multi-state operations | Highest cost, lowest internal burden |

When Each Option Stops Working

Manual payroll becomes unmanageable quickly. Once you have more than a handful of employees — or anyone with variable hours, commissions, or benefits — the error risk outpaces the cost savings.

Payroll software is efficient, but it doesn't make you compliant. Intuit's own disclosures note that QuickBooks Payroll users may need state agency websites for certain forms, withholding information, and employer registration requirements. The software runs the calculations; compliance responsibility stays with the employer.

That's where outsourcing to a firm like Tax Resolution Group — which handles both payroll processing and tax resolution — makes particular sense:

- Your business operates across multiple states

- You've received IRS notices related to payroll taxes

- You have complex compensation structures (commissions, bonuses, owner-employee arrangements)

- You want payroll integrated with your bookkeeping and tax planning rather than treated as a standalone function

Businesses dealing with existing payroll tax debt alongside an ongoing payroll need often benefit most from a firm with combined expertise — a software tool can't negotiate penalty abatement or represent you before the IRS.

Common Payroll Processing Mistakes and How to Avoid Them

Payroll errors carry real financial consequences. According to a 2022 EY survey reported through BusinessWire, one in five U.S. payrolls contains errors, with each error costing an average of $291. At scale, that adds up fast.

The Most Common Errors

- Worker misclassification — the IRS can assess employment taxes retroactively if contractors should have been classified as employees, and misclassified workers lose FLSA wage and overtime protections

- Overtime miscalculation — bonuses and commissions must be factored into the "regular rate" before calculating overtime; skipping this step is one of the most common FLSA violations

- Late W-4 implementation — not updating withholding within the required 30-day window after receiving a new form

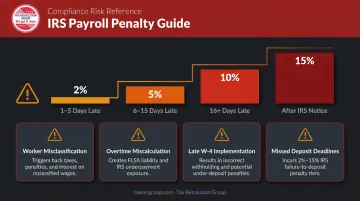

- Missing deposit deadlines — IRS failure-to-deposit penalties run in tiers: 2% for deposits 1–5 days late, 5% for 6–15 days late, 10% for more than 15 days late, and 15% if unpaid after a first IRS notice or demand for immediate payment

The Real Stakes

The IRS Data Book for FY 2025 reported 4,457,891 employment-tax civil penalty assessments totaling approximately $1.15 billion. Federal tax deposit penalties alone accounted for over 1.2 million assessments and nearly $118 million. These aren't edge cases — they represent ordinary businesses that fell behind on deposits or made filing errors.

The more serious exposure is personal. Under the Trust Fund Recovery Penalty (TFRP), when withheld employee taxes — income tax, Social Security, Medicare — aren't remitted to the IRS, the agency can hold any "responsible person" personally liable for the full unpaid balance. The business entity provides no shield here.

The Growth Problem

Those penalties often trace back to a simple root cause: businesses running payroll the same way they set it up when they had three employees. What worked then doesn't scale. A 30-person company with employees in multiple states, a mix of salaried and hourly workers, and a 401(k) plan has materially different compliance requirements than a startup. Regularly checking whether your payroll process still fits your business isn't optional — it's part of managing risk.

Conclusion

Payroll processing is a compliance-driven, legally regulated process that touches employee trust, cash flow, and your standing with the IRS. Get it wrong, and the costs compound fast — in penalties, back taxes, and damaged employee confidence.

Understanding the full cycle — from data collection and gross pay calculation through tax remittance and recordkeeping — gives you the tools to:

- Catch errors before they become IRS penalty notices

- Choose the right processing approach for your actual business size

- Stop treating payroll as a low-priority task with low-priority consequences

If your payroll has grown more complex, you've received IRS correspondence about employment taxes, or you're simply not confident the current process is airtight, that's the moment to bring in a professional. Tax Resolution Group offers payroll and tax resolution services from the same CPA-led team, so you're not managing two separate vendor relationships when a payroll issue becomes a tax problem.

Frequently Asked Questions

What are the 5 basic steps in processing payroll?

Collect employee hours and classification data, calculate gross pay, apply mandatory and voluntary deductions to arrive at net pay, disburse payment and issue pay stubs, then remit payroll taxes to the IRS and file required returns. Each step must be completed in sequence — errors early in the process carry forward.

What is the meaning of payroll processing?

Payroll processing is the complete operational cycle an employer uses to calculate employee earnings, apply deductions and withholdings, distribute net pay, and meet all federal and state tax filing and remittance obligations.

What are the 4 types of payroll systems?

Manual processing (spreadsheets), in-house payroll software, outsourced payroll to an accountant or payroll firm, and managed/full-service payroll providers. Manual keeps costs low but introduces higher error risk; managed services provide the strongest compliance support, typically at a premium price point.

Is payroll processing difficult?

The mechanics are learnable, but the complexity comes from keeping up with changing tax rates, multi-state regulations, deposit schedules, and worker classification rules. Errors carry financial penalties, which is why many businesses outsource payroll once they grow beyond a handful of employees.

What happens if payroll is processed incorrectly?

Consequences include IRS penalty notices, back-tax assessments, interest charges, employee disputes, and potential DOL investigations. The IRS failure-to-deposit penalty alone can reach 15% of unpaid taxes — and delays in correcting errors make the resolution significantly more costly.

How often should payroll be processed?

The most common cycles are weekly, biweekly, semimonthly, and monthly. State law may set minimum pay frequencies, and workforce type matters — hourly workers generally prefer shorter cycles. More frequent pay periods increase processing costs but ease financial pressure on employees.