That's the core problem. Bookkeeping gets treated as a back-office chore — something to deal with eventually — until "eventually" arrives in February with a pile of bank statements and a filing deadline. At that point, the financial damage is already done: missing receipts, unrecorded transactions, miscategorized expenses, and a tax preparer who now has to do cleanup work before they can do tax work.

This article covers the specific, practical ways that good bookkeeping changes tax prep outcomes for small businesses — faster filing, more deductions captured, and far less exposure to IRS complications.

Key Takeaways

- Clean, categorized records make tax filing faster and reduce costly filing errors.

- Organized expense tracking throughout the year is the most reliable way to capture every deduction.

- Businesses with accurate books can respond to IRS notices quickly and without scrambling.

- Neglecting bookkeeping compounds costs: missed deductions, penalty exposure, and inflated year-end accountant fees.

- Year-round bookkeeping consistently delivers better tax outcomes than catching up before the deadline.

What Good Bookkeeping Actually Means

Good bookkeeping isn't just keeping receipts in a folder. It's the consistent, accurate recording and categorization of every financial transaction a business makes:

- Income and expenses recorded as they occur

- Payroll tracked and reconciled each pay period

- Assets and liabilities reflected accurately on the balance sheet

- Bank statements matched against internal records regularly

A folder of receipts isn't bookkeeping. Bookkeeping is what happens when those receipts are entered, categorized, reconciled against bank statements, and organized into financial reports that reflect what's actually happening in the business.

Bookkeeping is also not a once-a-year task. It's a continuous process feeding into financial statements, cash flow management, and tax preparation. Businesses that treat it as ongoing infrastructure — rather than a pre-April scramble — arrive at tax season with nothing left to do except file.

IRS Publication 583 frames the purpose clearly: records help businesses monitor financial progress, identify income sources, track expenses, and prepare accurate tax returns. That's not a bureaucratic obligation — it's reason enough to keep organized books year-round.

Three Tax Prep Advantages of Good Bookkeeping

The advantages below aren't abstract. Each one maps directly to something measurable: time spent on tax prep, dollars of deductions captured, and exposure to IRS complications.

Faster and More Accurate Tax Filing

When financial records are organized, categorized, and current throughout the year, tax preparation becomes a documentation exercise rather than a detective exercise. The accountant works from clean data instead of hunting down missing receipts or reconstructing months of unrecorded transactions.

Good bookkeeping creates this advantage through three habits:

- Consistent transaction recording — every income and expense entry is logged as it occurs

- Regular bank reconciliations — account balances match actual bank activity on a monthly basis

- Current financial statements — profit & loss, balance sheet, and cash flow reports are always up to date

The IRS identifies four small business tax errors worth knowing: underpaying estimated taxes, making late deposits of employment taxes, filing late, and failing to separate business from personal expenses. Three of those four are directly preventable with organized bookkeeping.

The time cost is real. NSBA's 2024 survey on taxation found that 58% of small business owners spend more than 40 hours per year on federal taxes, with 28% spending more than 80 hours. That workload doesn't shrink when records are disorganized — it grows, because time that should go toward the return itself goes toward reconstructing records that should have already existed.

Businesses with high transaction volumes, multiple revenue streams, or seasonal income patterns feel this most acutely. The more complex the financials, the more expensive disorganized records become to untangle.

Maximizing Deductions and Lowering Tax Liability

One of the most direct financial benefits of good bookkeeping is deduction capture. Office supplies, business meals, vehicle use, home office costs, software subscriptions, professional services — every deductible expense needs a record created at the time of the transaction, not reconstructed afterward.

When expenses are categorized correctly throughout the year, there's a complete, defensible record of every deductible item. When they aren't, legally available deductions go unclaimed — not because the business didn't qualify, but because the documentation doesn't exist.

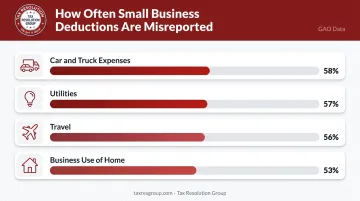

GAO data illustrates the scale of the problem. Among sole proprietors, misreporting rates for common deduction categories include:

- Car and truck expenses — 58% misreporting rate

- Utilities — 57% misreporting rate

- Travel — 56% misreporting rate

- Business use of home — 53% misreporting rate

These aren't fringe categories. They're the expenses most small business owners encounter regularly. Misreporting in these areas doesn't always mean fraud — it frequently means missing or incomplete documentation that can't support the deduction claimed.

Solid documentation discipline also unlocks better in-year planning. When a business owner can see categorized expenses in real time, they can time major purchases strategically, adjust estimated tax payments, and identify opportunities before the tax year closes — not after.

This is especially valuable for businesses in industries with high operating costs: media and entertainment companies, contractors, IT service firms, and any business with significant vehicle, equipment, or professional service expenses. For Tax Resolution Group clients in these sectors, tracking deductible costs with proper documentation throughout the year is a core part of the engagement — not an afterthought at filing time.

Audit Readiness and IRS Compliance

The IRS requires businesses to keep records as long as necessary to prove income or deductions on a tax return, with employment tax records retained for a minimum of 4 years. In an audit, the ability to produce organized, accurate documentation is the difference between a quick resolution and a prolonged, expensive process.

Good bookkeeping creates an audit trail that can be produced on demand:

- Organized ledgers with clearly categorized transactions

- Reconciled bank statements that match reported figures

- Receipts tied to specific expense entries

- Financial statements that align with the filed return

Clean books also reduce the likelihood of scrutiny in the first place. Many IRS notices stem from mismatched figures — income on 1099s that doesn't reconcile with the return, or deductions that can't be traced to supporting documents. Accurate records eliminate those gaps before they become problems.

The businesses with the most to gain here are those claiming home office deductions, significant vehicle expenses, or inconsistent revenue patterns. These are the categories GAO flagged for high misreporting rates — and the ones IRS examiners focus on when reviewing Schedule C returns.

What Happens When Bookkeeping Is Neglected

The most common scenario plays out like this: a small business owner arrives at tax season with incomplete records and asks their accountant to figure it out. The accountant then spends hours — billable hours — reconstructing transactions from bank statements, chasing down receipts, and reconciling months of activity that should have been done continuously throughout the year.

That reconstruction work creates several compounding problems:

- Expenses that weren't recorded or categorized can't be confidently claimed without documentation, meaning deductions get left on the table

- Reconstructed records are more likely to contain inaccuracies, which increases the risk of IRS notices and audits

- The IRS underpayment interest rate for Q3 2026 is 7%, with failure-to-file penalties reaching up to 25% of unpaid tax and failure-to-pay penalties adding 0.5% per month

- Tax preparers who must clean up disorganized records before filing charge for both tasks — not just one

There's also a cost that doesn't show up on any invoice. A business owner who discovers in April that they missed six months of deductible vehicle expenses can't recapture those deductions with the same confidence as someone who logged every trip in real time.

That gap — between what was deductible and what can actually be proven — is where neglected bookkeeping does its most lasting damage.

How to Get the Most Value from Bookkeeping Year-Round

Bookkeeping produces its maximum value when applied consistently — not in bursts before deadlines. Here's what that looks like in practice:

Monthly:

- Reconcile all bank and credit card accounts

- Categorize and record all transactions

- Review accounts receivable and payable for accuracy

Quarterly:

- Review financial reports (profit & loss, balance sheet)

- Check estimated tax payments against current income

- Identify any categorization errors before they compound

- Catch tax planning opportunities while the year is still open

Year-end:

- Confirm all accounts are reconciled

- Verify payroll records and 1099 obligations

- Prepare supporting documents for the tax preparer

Tools like QuickBooks can streamline this process by automating transaction categorization, syncing bank accounts, and generating the financial reports tax preparers need.

Tax Resolution Group has deep familiarity with QuickBooks and can help configure the system correctly from the start, since a poorly configured setup produces unreliable data that undermines the entire bookkeeping process.

Firms that get the most from their bookkeeping treat it as a strategic function rather than a year-end compliance obligation. Tax Resolution Group's general ledger management and review service exists precisely for this reason: regular reviews catch discrepancies early, before errors cascade through financial statements and create problems at tax time.

Conclusion

Good bookkeeping shapes tax preparation in ways that compound quietly throughout the year — not just in the final weeks before a filing deadline. Knowing where every dollar went, keeping records organized, and sustaining those habits consistently means tax season stops being a scramble.

The advantages — faster filing, more deductions captured, and genuine audit readiness — don't appear all at once. These benefits build over time. Businesses that maintain organized financial practices year after year see more return each tax season, because clean records become the norm rather than something to chase.

Bookkeeping isn't a regulatory burden. It's the ongoing practice that directly protects a small business's bottom line and keeps financial risk at a level that's actually controllable.

Frequently Asked Questions

Why is bookkeeping important for a small business?

Bookkeeping gives small business owners an accurate, ongoing picture of their financial position. It directly affects tax compliance, deduction capture, and cash flow management — and it's the foundation for making informed business decisions throughout the year, not just at tax time.

Does QuickBooks help with taxes for small businesses?

Yes. QuickBooks automates transaction tracking, categorizes expenses, reconciles bank accounts, and generates the financial statements tax preparers need. When configured correctly, it makes the handoff to your tax preparer faster and reduces filing errors.

How often should I update my bookkeeping records to stay tax-ready?

At minimum, monthly — ideally weekly. Regular updates keep reconciliations current, help catch errors before they compound, and ensure all transactions are documented before receipts are lost or details are forgotten.

What bookkeeping records do I need to give my accountant at tax time?

Core documents your accountant needs:

- Profit and loss statement

- Balance sheet

- Cash flow statement

- Bank reconciliations

- Payroll records

- Categorized expense receipts

If bookkeeping was maintained throughout the year, all of these should already be organized and ready.

Can good bookkeeping actually reduce my tax liability?

Yes. Organized bookkeeping ensures no legitimate deduction goes unclaimed, which directly reduces taxable income. Categorizing expenses in real time throughout the year is how businesses consistently capture every deduction they qualify for — not just the obvious ones.

What happens if my bookkeeping is inaccurate when I file taxes?

Inaccurate books lead to filing errors — and those errors can trigger IRS notices, underpayment penalties, and interest charges. In an audit, the IRS can disallow any deduction you can't substantiate with documentation, adding tax assessments on top of existing penalties.