Introduction

Getting your IRS agreement approved feels like crossing the finish line. It isn't.

Once an installment agreement, Offer in Compromise (OIC), or Currently Not Collectible (CNC) status is formally accepted, a new phase begins with its own rules, deadlines, and consequences that most taxpayers never see coming.

Miss a single payment. Forget to file one return. Let a new tax balance go unaddressed. Any of these can void your agreement and restart the collection process from scratch.

Those risks are exactly why post-agreement compliance matters as much as getting approved in the first place. Most guidance on tax resolution focuses on getting an agreement. This article covers what happens after — the compliance obligations, IRS monitoring, and common mistakes that determine whether your resolution actually holds.

Key Takeaways

- Agreement acceptance starts a compliance period, not the end of your IRS obligations

- OIC agreements require five years of strict filing and payment compliance after acceptance

- The IRS automatically keeps any tax refund owed for years covered by an accepted OIC

- Missing one payment triggers a CP523 default notice with a 30-day response window

- New tax balances cannot be folded into an existing agreement and must be handled separately

What Happens Immediately After Your IRS Agreement Is Approved

The IRS sends a formal notice confirming your agreement type, payment terms, and the date your compliance obligations begin. For installment agreements, this typically arrives as Letter 2273-C or Letter 3217-C.

For accepted Offers in Compromise, the IRS issues Form 7249, Offer Acceptance Report — documenting the acceptance date, liabilities covered, the agreed offer amount, and payment terms. Read it carefully. Every obligation you carry for the life of the agreement is spelled out in that document.

Three immediate action items follow from that notice.

Step 1: Confirm Agreement Terms and Payment Setup

Verify the payment amount, due dates, and accepted payment method. The IRS accepts payments through EFTPS, direct debit, check, money order, and payroll deduction — the available options vary by agreement type.

Set up automated payments wherever possible. Manual payments introduce human error into a process that has zero tolerance for it.

Step 2: Understand What the IRS Will Keep

If your OIC was accepted, the IRS automatically retains any tax refund — including interest — for all tax years through the date the offer was accepted. This is not a penalty. It is a standard condition written into Form 656.

Critically, retained refunds are not applied toward your offer balance. You still owe the full agreed amount. Don't count on a refund to cover an upcoming offer payment — budget for each installment independently.

Step 3: Federal Tax Lien Status After Agreement

An existing federal tax lien does not disappear when your agreement is accepted.

- Installment agreements: The lien typically remains until the debt is paid in full

- OIC agreements: The lien is released once the full offer amount is paid — timing varies by payment method:

- Cashier's check, money order, or online payment: immediately upon receipt

- Personal or business check: 30 days after receipt

- Credit card: 120 days

- General guideline from the Form 656 Booklet: liens are released within 45 days after final payment is received and verified

One important distinction: for streamlined installment agreements under $50,000, the IRS generally does not file a new Notice of Federal Tax Lien. If you're concerned about credit impact or have an upcoming property transaction, this threshold matters.

Your Ongoing Compliance Obligations After the Agreement

The compliance period is where most agreements actually fail.

For installment agreements, compliance is required for the entire life of the agreement — which can span years. For OIC agreements, IRS Form 656 terms require five full years of strict compliance from the acceptance date.

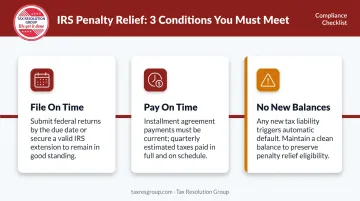

"Compliance" means three things:

- File on time: all federal tax returns, including business returns if applicable, must be filed by their due dates (extensions count if filed properly)

- Pay on time: all tax payments, including quarterly estimated taxes, must be made when due

- No new balances: any new unpaid federal tax liability is a default trigger, not an add-on

Filing and Estimated Tax Obligations

Failing to file even one return during the compliance period can trigger default. This applies to both individual and business taxpayers — there are no exemptions for complex returns or unusual circumstances.

Self-employed taxpayers face a specific risk here. If your income isn't subject to withholding, you're required to make quarterly estimated tax payments. Underpaying those payments creates a new tax liability. That new liability can void your entire agreement — even if you've made every installment payment perfectly.

If you're self-employed, set quarterly payment reminders and calculate estimates conservatively — underpaying by even a small amount can unravel years of compliance progress.

New Balances and Contact Information

Any new tax balance arising during the agreement period must be paid separately and in full. For OIC specifically, you cannot set up an installment arrangement on a new liability — it must be resolved immediately.

Staying reachable matters just as much as staying current. Update your address with the IRS any time you move, using Form 8822. The IRS sends notices to your last known address, and a missed notice due to an outdated address can result in a compliance violation you don't discover until collection action has already resumed.

How the IRS Tracks Compliance Post-Agreement

The IRS doesn't simply trust that you'll comply. There's an active monitoring structure in place.

For accepted OICs, the Monitoring OIC Unit in Compliance Services tracks post-acceptance activity. The IRS uses the Automated Offer in Compromise (AOIC) system alongside IDRS transaction codes to record and monitor compliance from acceptance through closure.

For installment agreements, payment records are cross-referenced against your account automatically. A missed or late payment typically triggers an automated notice before formal default proceedings begin.

Understanding the CP523 Notice

IRS Notice CP523 is titled "Notice of intent to levy" and "Intent to terminate your installment agreement." It signals that the IRS did not receive a required payment or that another default condition was triggered.

Response window: 30 days from the notice date.

That deadline is firm. If you don't cure the default within 30 days, the IRS can terminate the agreement and resume collection — including levies.

At that point, reinstating the agreement requires a separate request — and there's no guarantee the IRS will approve it. Tax Resolution Group helps clients stay ahead of that risk by monitoring payment deadlines, responding to IRS notices, and resolving compliance issues before a CP523 ever arrives.

Common Mistakes That Put IRS Agreements at Risk

Treating the Agreement as "Done"

The most costly mistake is passive compliance — assuming everything is on autopilot and stopping active monitoring. Even one missed payment restarts the entire collection process. Check your bank statements, confirm payment receipts, and stay actively on top of every transaction.

Expecting New Balances to Roll Into the Existing Agreement

This doesn't happen. A new unpaid federal tax balance is a default trigger — not an automatic addition to your installment plan. Taxpayers who assume a new liability can wait often find their entire agreement in default by the time they respond. Address new balances as soon as they arise.

Relying on IRS Confirmation Alone

Keep your own records of every payment: confirmation numbers, bank statements, transaction dates. IRS processing errors do occur. If the IRS applies a payment incorrectly or fails to record it, your documentation is what protects you.

Misunderstanding Penalties and Interest During the Agreement

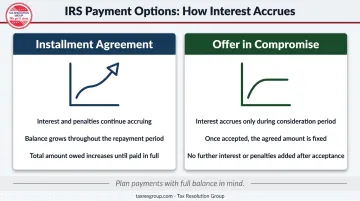

Penalties and interest behave differently depending on your agreement type:

- Installment agreements: The Taxpayer Advocate Service confirms that interest and penalties continue to accrue until the balance is paid in full

- OIC agreements: Interest accrues while the offer is under consideration; once accepted, the agreed amount is fixed — but you still owe that amount in full

Plan your payments with the full balance in mind, not just the principal.

What to Do If Your Situation Changes After an Agreement

Financial circumstances shift — and the IRS has limited but real options when they do.

Modifying an Installment Agreement

If your financial situation worsens, you may request a lower payment amount or a temporary deferral. The IRS Online Payment Agreement tool allows eligible taxpayers to revise existing plans online. For more complex modifications, contact the IRS before missing a payment — not after. Calling proactively signals good faith and preserves more options.

OIC Payment Extension

For Offer in Compromise agreements, the IRS may grant a one-time payment extension within a 24-month period. Use this option sparingly — once the extension ends, payments must return to the regular schedule immediately.

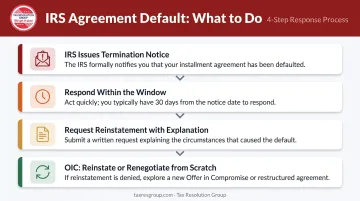

If Your Agreement Defaults

If you miss the window to cure a default after a CP523 notice:

- The IRS issues a notice of intent to terminate

- You have a window to respond and request reinstatement

- Reinstatement requires a valid explanation for the non-compliance and may involve additional conditions or fees

- An OIC that defaulted due to failure to maintain filing and payment compliance cannot be modified — it must be reinstated or renegotiated from scratch

Act quickly. Options narrow fast once the agreement is formally terminated.

Conclusion

Reaching an IRS agreement is a real milestone. But it's the compliance period that determines whether that resolution actually holds.

Taxpayers who convert an agreement into lasting financial relief treat the post-agreement phase as seriously as the negotiation itself. That means staying on top of four things:

- Tracking payments independently, not waiting for IRS confirmation

- Filing on time without exception, every year

- Addressing new tax obligations as they arise

- Responding to IRS notices before deadlines pass

Staying ahead of your obligations — rather than reacting to problems — is what makes the difference between a resolution that holds and one that unravels. If you're navigating the post-agreement phase and have questions about your obligations, Tax Resolution Group can help you stay on track.

Frequently Asked Questions

What is the tax resolution process?

Tax resolution is the process of negotiating with the IRS to settle or manage unpaid tax debt through formal programs — installment agreements, Offers in Compromise, or Currently Not Collectible status. Reaching an agreement is only part of the process; maintaining ongoing compliance is what keeps it in force.

How long does a tax resolution take?

Installment agreements can be set up in weeks; an OIC investigation can take up to 24 months depending on case complexity. Post-agreement compliance extends the total timeline further — five additional years for OIC recipients, or the full life of the payment plan for installment agreements.

How long does it take for the IRS to process an installment agreement?

Online applications for qualifying balances are often approved within minutes. Mail submissions or cases handled through a representative may take up to 30 days for IRS review. Processing time does not pause interest and penalties — they continue accruing throughout.

How long does it usually take after an IRS letter gets resolved for my refund to come?

Active OIC recipients don't receive standard refunds — the IRS retains any refund for tax years covered by the offer. In other resolved cases with no offset, refunds follow the standard window; check IRS Where's My Refund and any Bureau of the Fiscal Service offset notices for your status.

What happens if I miss a payment after my IRS agreement is approved?

Missing a payment can trigger a CP523 notice — the IRS's intent to terminate your installment agreement. You have 30 days from the notice date to respond and cure the default. After that window closes, the IRS can terminate the agreement and resume collection action.

Can the IRS change the terms of my agreement after it is accepted?

The IRS cannot unilaterally change accepted terms, but it can default the agreement if you violate its conditions. OIC terms are fixed once accepted and cannot be amended. Installment agreements may be modified upon request if your financial circumstances change materially.